by Taylor Anderson | Jun 26, 2025 | Industry, News Feed

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

EXp founder Glenn Sanford fired back at Compass on Wednesday, two days after being mentioned in a lawsuit Compass filed against Zillow, as the battle between brokerages continues to roil.

Sanford blasted recent consolidation moves, and the push for private listings that has become a flashpoint in the industry.

Glenn Sanford | eXp Realty

“This isn’t about any single company’s business model,” Sanford wrote on LinkedIn. “It’s about whether real estate maintains a competitive landscape where innovation can emerge from anywhere, or becomes dominated by a handful of capital-intensive players controlling listing access.”

Compass has used both consolidation and private listings to sustain its growth as the No. 1 brokerage in the nation by sales volume.

But as the founder of the No. 1 brokerage in the nation by total transactions, Sanford used his LinkedIn post to distinguish eXp from Compass and call for continued support of broad access to listings via multiple listing services.

“EXp handles more transactions than any other brokerage in the United States,” Sanford, who today serves as CEO of eXp parent eXp World Holdings, wrote. “We’re now large enough that we could create our own private marketplace and walled gardens. But we choose not to.”

Robert Reffkin

The post was eXp’s first public response after Compass mentioned it in a lawsuit filed against Zillow on Monday over the portal’s new policy banning listings if they’re marketed off-MLS for more than 24 hours.

When Zillow announced the policy in April, eXp was quick to come out in support of it. Compass said that support amounted to conspiracy between Zillow and eXp. (EXp was not named as a defendant in the lawsuit.)

Compass is working to uphold its “3-Phased Marketing Strategy,” which includes a Compass Private Exclusive period where sellers privately market a property without listing it on an MLS.

In its suit, Compass revealed that nearly half of all the brokerage’s homeseller clients outside Washington state (48.2 percent) opted to start by marketing their homes as private exclusives during the first three months of the year, though most (94 percent) eventually list their homes on the MLS as well. The suit also argued that Zillow is a monopoly, forcing consumers to market their homes in a way that the portal wants so it can monetize the listing.

As part of its ban, Zillow has said public marketing includes yard signs, social media posts and brokerage private listing networks (PLN) where consumers must log into a site to see listings.

Compass CEO Robert Reffkin said his company sued Zillow to protect consumer choice.

“This lawsuit is about protecting consumer choice. No one company should have the power to ban agents or listings simply because they don’t follow that company’s business model,” Reffkin said in a statement. “That’s not competition. It’s coercion. Imagine if Amazon banned a seller for offering a product on their own website first. That’s what Zillow is doing in real estate. Consumers should have the right to choose how they sell their homes.”

The battle for private listings

The battle between Compass, Zillow and eXp, among others, gets to a key dividing line in the industry around when, where and how real estate listings are marketed.

Supporters of policies that have maintained broad public access to listings, including via Zillow and other real estate portals, say that it is unique and fosters competition among real estate companies.

In an exclusive interview on Wednesday, eXp Realty CEO Leo Pareja, speaking by phone from Barcelona, Spain, said broad access to listings via public portals and other websites made the industry in the U.S. far more streamlined than in most other countries.

Leo Pareja

“We as Americans take for granted the beauty of the efficient market that we enjoy in the U.S. and Canada,” Pareja said. Without access to listings via the MLS and other sources, Pareja added, “The process would be very difficult. It would take you six to 10 websites to maybe have an idea of what the inventory looks like. And months and months of hunting and pecking — no transparent market.”

Alternatively, Compass has argued that its three-phased plan allows consumers to test the market for pricing, gain insights into aspects about the home and drum up buyer interest. The second phase involves marketing the listing on Compass.com as a “Coming Soon” listing, a status that doesn’t show price history or days on market. The final stage is listing the home on the MLS.

In response to Sanford’s LinkedIn post, a Compass spokesperson pointed out that eXp previously launched its own exclusive listing system.

“Compass is confused by eXp Founder’s statement that they ‘choose not to’ launch an off-MLS listing system because in 2023 eXp launched an off-MLS listing system called eXp Exclusives,” the spokesperson told Inman.

In October 2023, Pareja said eXp believed marketing on the MLS was the “highest and best form” of marketing a home for sale, but that there were “situations where sellers may not want to enter the property into an MLS due to restrictions on showing it and many other unique scenarios.”

He specifically mentioned new-builds that aren’t yet finished, tenant-occupied rentals, or “properties whose sellers are just not comfortable entering into the MLS but would sell if they received an offer that satisfied their needs and worked with their requirements.”

Taking on Zillow

Asked about Compass’ battle with Zillow, one industry insider noted that Zillow became a behemoth that now generates substantial revenue selling consumer leads to agents via listings it gets through the MLS.

Victor Lund

“What I see happening as a result of Compass picking a fight with Zillow is that more agents join Compass, because Compass is standing up for agents,” said Victor Lund, a managing partner of Wav Group.

On Sanford’s post, Lund said that the entrepreneur was “spinning a narrative.”

“Which by the way is what all of them are doing,” Lund said. “These are all public companies that are spinning a narrative that is capturing the capital markets as well as their agents.”

NextHome CEO James Dwiggins, who has been critical of Compass’ private listings push, said that if another major brokerage and franchiser followed Compass’ lead and launched its own private listings network where it had almost 50 percent of its inventory off MLS, it could have a domino effect on the industry.

James Dwiggins | NextHome

“What ends up happening is that everybody has to respond in kind in order to keep their people so they don’t lose their agents,” Dwiggins said. “And all of the big companies launch their private listing networks, which is what you saw with Douglas Elliman and Corcoran.”

“It would be catastrophic,” he added, “and be so harmful to consumers.”

Email Taylor Anderson

by Verl Workman | Jun 26, 2025 | Industry, News Feed

By focusing on lead generation, networking, productivity and skill development, coach Verl Workman writes, you’ll rise above the pack and become the driving force behind your team’s success.

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

In nearly every industry, including real estate, standing out and becoming a rainmaker on your team requires more than just hard work. It involves strategic thinking, continuous development and a proactive approach to both business and people.

TAKE THE INMAN INTEL INDEX SURVEY FOR JUNE

Rainmakers are the top producers, the ones who consistently generate leads, close deals and drive business growth. If you want to elevate your career and become a key player on your team, here’s how to do it.

1. Understand your role beyond selling homes

Being a successful real estate agent isn’t just about closing deals; it’s about creating opportunities. A rainmaker identifies and capitalizes on new business prospects, whether through networking, strategic marketing or leveraging referrals. You must become a market expert, knowing trends, pricing strategies and buyer behaviors better than anyone else on your team.

I also recommend that you “serve regardless of opportunity.” Offer prospects resources of value for the sake of helping them, not just to get them to become a client.

Action steps:

- Actively seek out new listings and potential buyers. Prospect!

- Study the market trends and neighborhood developments. Be the go-to expert on all things real estate.

- Position yourself as a go-to resource by providing valuable insights to clients and colleagues.

- Always be willing to offer something of value, sometimes this shows up as options. Be an options broker by providing the best options and allowing the client to be in a position to make the best decision for them, without regard to how it impacts you.

2. Build and nurture

A rainmaker’s strength lies in their networking abilities. The more people who know you as an expert, the more referrals and deals you’ll generate. Focus on building strong relationships with past clients, potential buyers, industry professionals and community leaders.

Action steps:

- Attend and lead local events, and make connections with homeowners and business owners.

- Leverage social media and digital marketing to engage with your audience. Keep balance in your posts: family, business, fun, friends.

- Stay top of mind with past clients by offering market updates, home tips and personal touches, like holiday cards, anniversary of the home purchase and check-in calls.

- Conduct your own “Lunch and Learns” or webinars around real estate-specific topics for first-time buyers, investors or multigenerational homes.

3. Adopt daily success habits (DSH)

Success in real estate comes from consistency. Developing daily success habits focused on money-making activities (MMAs) will separate you from the pack. This means committing to lead generation, follow-ups, showings and strategic planning every single day. I always recommend using not only a Daily Success Habits Tracker, but also something I call the “My Perfect Week Scheduler.”

In prospecting, the ultimate source of power is action. When you measure what you do daily (awarding points for money-making activities), you become clear on how much time you spend focused on activities that generate revenue. A rainmaker makes course corrections and makes MMAs non-negotiable in their daily routine.

Action steps:

- Use a daily success habits (DSH) tracker to measure your productivity.

- Dedicate time each morning to prospecting and lead follow-up.

- Establish a structured routine that prioritizes high-impact activities, such as calls, client meetings and negotiations.

4. Leverage systems and tools

The best rainmakers work smarter, not harder. They use systems to track leads, automate follow-ups and manage transactions seamlessly. By incorporating technology and data-driven tools, you can streamline your workflow and increase conversions.

Action steps:

- Utilize CRM software such as Boldtrail, CINC, Follow Up Boss, BoomTown or WSS Lead Tracking to manage leads effectively.

- Automate follow-ups with email drip campaigns and text reminders.

- Maintain an active and organized contact list to ensure that no leads fall through the cracks. Follow the ABC Lead System for higher conversion.

- Maintain a “Top 50” list with 50 people who know, like and trust you. Reach out to them monthly with a personal touch, and ensure they know you are counting on them for at least one referral per year.

5. Create a culture of productivity on your team

Rainmakers don’t just succeed individually — they lift others. A truly valuable agent supports, mentors and encourages their team members. By fostering a culture of collaboration and productivity, you’ll naturally establish yourself as a leader.

Action steps:

- Share knowledge, tips and strategies with your team. Teach them to hunt, and demand excellence in everything they do: prospecting, follow-up, presentation skills and client care.

- Implement daily team huddles to review goals and challenges.

- Practice scripts and dialogs for a minimum of 30 minutes a day.

- Prospect as a team for at least 1 hour daily.

- Deliver a positive and energetic work atmosphere by celebrating wins and victories. Step in and help each member of the team personally and professionally.

6. Set ambitious goals and track your progress

A rainmaker always aims higher. Whether it’s closing 50 transactions in a year or expanding into luxury real estate, setting clear and ambitious goals will keep you motivated and focused. Nobody ever accomplished anything significant by setting SMART goals.

If you incorporate the words realistic and attainable into your goal-setting practice, you will never achieve anything exceptional, amazing or out of this world. It’s time to set some STUPID goals. STUPID goals are

- Strategic

- Transformational

- Unrealistic

- Purpose-driven

- Innovative

- Dynamic

Remember, if your vision doesn’t scare you, it’s not big enough!

Action steps:

- Define your STUPID goals.

- Break down your massive, ambitious goals into manageable action steps. Then do the work. It’s OK to fail if failing means you are kicking butt and doing better. I call it failing up.

- Regularly review your progress, and adjust strategies as needed.

7. Be a lifelong learner

The real estate industry is constantly evolving, and the best agents never stop learning. Staying ahead of industry changes, marketing trends and negotiation techniques will ensure you remain a top producer. You can accomplish this using what I call the 3-2-1 system. Call three past clients every day, prospect until you add two new prospects into your database, and learn one new thing every day. You will be blown away at how your business grows and your knowledge grows with it.

Action steps:

- Attend real estate workshops, coaching programs and industry conferences.

- Read books, listen to podcasts, and follow top-performing agents for inspiration and insights.

- Hire a team and leadership coach. High performers in every business and sport have specialty coaches who can look at your performance and make course corrections.

8. Become a closer and deal maker

Closing deals is what sets a rainmaker apart — the ability to find and convert leads into clients and clients into closed transactions. Mastering the art of prospecting, serving, negotiation and relationship-building will elevate you to the top of your field.

Action steps:

- Develop effective sales scripts tailored to various client scenarios.

- Learn advanced negotiation strategies to effectively handle objections.

- Follow up persistently — many deals are won through consistent outreach and engagement.

Become the rainmaker your real estate team needs

Becoming a rainmaker in real estate isn’t about luck — it’s about deliberate action, consistency and relentless improvement. By focusing on lead generation, networking, productivity and skill development, you’ll not only rise above the pack but also become the driving force behind your team’s success.

Start implementing these strategies today, and you’ll soon find yourself leading the charge in your market and becoming the leader you’d want to follow.

Verl Workman is founder and CEO of Workman Success Systems. Connect with him on LinkedIn or Instagram.

by Andrea V. Brambila | Jun 25, 2025 | Industry, News Feed

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

The jury trial for Compass’s antitrust case against Northwest Multiple Listing Service over listing display rules is now on the court’s calendar.

On Friday, June 20, Judge Jamal N. Whitehead of the U.S. District Court for Western Washington set the trial date for June 8, 2026, nearly a year from now.

Whitehead scheduled the trial for June 2026 as suggested by Compass, and over NWMLS’s objection in a June 16 joint status report that choosing a date would be “premature at this time.” The parties did agree that it was too early to ” determine the number of trial days necessary.”

Compass filed the suit in April, alleging Northwest MLS — a broker-owned MLS that Compass is itself a shareholder of — restrains consumer choice and broker competition by banning office exclusives. Office exclusives are listings that listing brokers market within their own brokerage and do not submit into the MLS for view by other real estate agents in the market. Such listings are a key component of Compass’s “3-Phased Price Discovery and Marketing Strategy” for homesellers.

NWMLS has not yet filed its motion to dismiss the case, but has argued that Compass’s office exclusives are “fundamentally unfair and perpetuate inequities that have long plagued the housing system,” and “will lead to the dismantling of the real estate marketplace for the exclusive benefit of those brokerage firms that choose to exploit them.” Compass has denied these allegations.

The parties have agreed that NWMLS will submit its motion to dismiss by June 30, 2025.

The trial date in this case was set at almost the same time that Compass filed yet another antitrust suit to defend its listing marketing strategy, against Zillow.

Read the joint status report (re-load page if document is not visible):

Read the case schedule (re-load page if document is not visible):

Email Andrea V. Brambila.

Like me on Facebook | Follow me on Twitter

by Matt Carter | Jun 25, 2025 | Industry, News Feed

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Economists and investors expect Federal Reserve policymakers to continue to resist calls by the Trump administration to lower interest rates until they see more data on how tariffs and other policies are impacting inflation and employment.

Grilled by House and Senate lawmakers at separate hearings this week, Fed Chair Jerome Powell defended the central bank’s reluctance to resume cutting rates, saying the job market remains solid and that there’s no rush to make a decision.

After the Fed voted unanimously on June 18 to hold rates steady, Associated Press Reporter Chris Rugabar asked Powell if “cracks in the jobs market” and housing data “that have been pretty weak” could justify future rate cuts.

“I think if you look at the overall picture, what you’re seeing is 4.2 percent unemployment, and an economy that’s growing at a rate [that] appears to be 1-1/2, 2 percent — maybe a little better than that,” Powell said.

TAKE THE INMAN INTEL SURVEY FOR JUNE

While consumer sentiment has “come up off of very low levels,” it’s still depressed, Powell acknowledged.

“The housing market is a longer run problem, and also a short run problem,” Powell said. “Basically, we have a longer run shortage of housing, and we also have high [mortgage] rates right now. I think the best thing we can do for the housing market is to restore price stability in a sustainable way and create a strong labor market.”

Trump took to social media after the vote and urged the Federal Reserve Board to “override this Total and Complete Moron!” referring to Powell. “Maybe, just maybe, I’ll have to change my mind about firing him?”

Vice President J.D. Vance and Federal Housing Finance Agency Director Bill Pulte kept up the heat on Tuesday, with Vance saying he’d “love to hear an argument for why Powell cut rates 50 points right before an election but can’t do it now with inflation lower.”

Pulte claimed Powell’s interest rate policies “are not based on data but instead on Powell’s politicization of the Fed,” calling them “dangerous.”

On Wednesday — a few hours before ordering Fannie Mae and Freddie Mac to study allowing homebuyers to count crypto holdings as an asset — Pulte called on Powell to resign.

Trump told reporters Wednesday that he already has “three or four people” in mind who might replace Powell — although it’s unclear whether he will try to fire him.

Trump appointed Powell to lead the Fed during his first term, and his term is not set to end until May 2026.

One reason the Trump administration has grown impatient with Powell is that inflation has been nearing the Fed’s 2 percent goal. The personal consumption expenditures (PCE) price index, the Federal Reserve’s preferred gauge of inflation, showed the price of goods and services rose 2.1 percent in April from a year ago, the Bureau of Economic Analysis reported last month.

But while the Fed can pull levers that give it direct control over short-term interest rates, mortgage rates are determined by investor demand for mortgage-backed securities (MBS), which fund most home loans.

As the Fed cut short-term interest rates by a full percentage point in its final three meetings of 2024, mortgage rates moved by about the same amount in the opposite direction, as incoming economic data suggested inflation was on the rise again.

The last time the Fed cut rates, mortgage rates went up

Powell has been saying for months that Fed policymakers need more time to assess the impacts of the Trump administration’s policies in areas including tariffs, immigration, taxes and regulation.

The “dot-plot” in the Fed’s latest Summary of Economic Projections shows members of the Federal Open Market Committee (FOMC) expect to cut the short-term federal funds rate just twice later this year, to between 3.75 percent and 4 percent.

“Lawmakers this week have been no more successful than journalists last week in getting Chair Powell to set out a more concrete timetable for the policy easing anticipated by a slender majority of [Fed policymakers] this year,” economists at Pantheon Macroeconomics said in their latest U.S. Economic Monitor.

The CME FedWatch Tool, which tracks futures markets to predict future Fed moves, shows investors think there’s only a 25 percent chance of a July rate cut. But bets placed by futures market investors as of June 25 put the odds of a September rate cut at 90 percent — up from 64 percent on June 18.

Fed policymakers will receive “substantial extra information” if they hold off until September to make a decision, Pantheon economists Samuel Tombs and Oliver Allen wrote Wednesday.

By September, “we think the FOMC will have seen a sequence of three weak labor market reports through August,” Tombs and Allen predicted, with the unemployment rate hitting 4.5 percent by August — 4 months sooner than currently projected by the Fed.

“That would represent a resounding call to ease policy, even before the full effect of the tariffs on inflation is visible in the data,” Pantheon forecasters wrote.

In the meantime, mortgage rates have been holding steady in the high sixes.

Mortgage rates stabilize

After hitting a 2025 low of 6.48 percent on April 4, rates on 30-year fixed-rate conforming mortgages have been rangebound between 6.75 and 7 percent in May and June, according to lender data tracked by Optimal Blue.

Weekly surveys of lenders by the Mortgage Bankers Association show that demand for purchase loans was up 12 percent last week from a year ago.

“Applications increased slightly overall driven by FHA refinances, but conventional applications saw declines over the week,” MBA Deputy Chief Economist Joel Kan said, in a statement. “The average loan size for purchase applications declined to $436,300, the lowest level since January 2025, driven by decreasing conventional purchase loan sizes.”

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

by Matt Carter | Jun 25, 2025 | Industry, News Feed

Head of Fannie Mae and Freddie Mac’s federal regulator says mortgage giants should consider what risk mitigation might be required when counting mortgage borrowers’ crypto holdings as an asset, “including adjustments for market volatility.”

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

The head of Fannie Mae and Freddie Mac’s federal regulator has directed the mortgage giants to consider allowing borrowers to count cryptocurrency as an asset without having to convert their holdings into dollars.

In a post on the social media platform X Wednesday — Federal Housing Finance Agency Director Bill Pulte’s preferred channel for issuing official communications — Pulte said cryptocurrency is “an emerging asset class that may offer an opportunity to build wealth outside of the stock and bond markets.”

TAKE THE INMAN INTEL SURVEY FOR JUNE

Pulte is a crypto investor himself — in addition to millions of dollars in annual dividends from his stakes in Pulte Group and several heating and air conditioning companies, he listed $500,000 to $1 million in bitcoin among the assets he disclosed in a financial disclosure statement for executive branch personnel.

The order Pulte issued Wednesday directs both Fannie and Freddie “to prepare a proposal for consideration of cryptocurrency as an asset,” but only in cases where the assets are “evidenced and stored on a U.S.-regulated centralized exchange.”

Bill Pulte

Fannie and Freddie must also consider what risk mitigation might be required when counting mortgage borrowers’ crypto holdings as an asset, “including adjustments for market volatility and ensuring sufficient risk-based adjustments to the share of reserves comprised of cryptocurrency,” Pulte said.

The mortgage giants were instructed to submit any proposed policy changes regarding the treatment of crypto to their board of directors for approval — Pulte chairs both Fannie and Freddie’s boards — before submitting them to FHFA for review.

Commenting on Pulte’s proposal, Annapolis, Maryland based mortgage banker John Downs said asset reserves are not as much of a factor in obtaining loan approvals as they used to be.

“That prevents the crypto rug from truly impacting the borrowers ability to repay,” Downs wrote, alluding to the dramatic ups and downs in crypto valuations.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

by Matt Carter | Jun 25, 2025 | Industry, News Feed

The 2023 order, aimed at ensuring the collection of information about applicants’ race, ethnicity and gender, wasn’t scheduled to be lifted until 2028. Regulators say the bank has fulfilled its obligations.

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

In its latest move to ease regulations, the Consumer Financial Protection Bureau (CFPB) has terminated a 2023 consent order with Bank of America aimed at addressing allegations that the lender reported false information about mortgage borrowers to federal regulators.

Bank of America was accused of failing to ask some mortgage applicants demographic questions about their race, ethnicity and gender as required by the Home Mortgage Disclosure Act (HMDA) — data that’s collected to uncover potential discriminatory lending patterns.

The CFPB claimed that in addition to failing to collect that demographic information from some borrowers, Bank of America falsely reported that the applicants had chosen not to respond.

Bank of America knew “that many loan officers receiving applications by phone were failing to collect the required data as early as 2013, but the bank turned a blind eye for years,” the CFPB alleged in announcing a $12 million settlement.

Under the terms of a Nov. 27, 2023, consent order, Bank of America also agreed to implement a compliance plan ensuring that it collected, recorded and reported required HMDA data used by the CFPB and other federal regulators to detect redlining.

While the consent order was to remain in effect for a minimum of five years — until late 2028, if no further reporting violations occurred — Office of Management and Budget Director Russell Vought on June 4 signed an order terminating it, saying Bank of America had fulfilled its obligations.

The CFPB did not publicize the action, which was first reported by Reuters this week. Bank of America declined Inman’s request for comment on the early termination of its consent order with the CFPB.

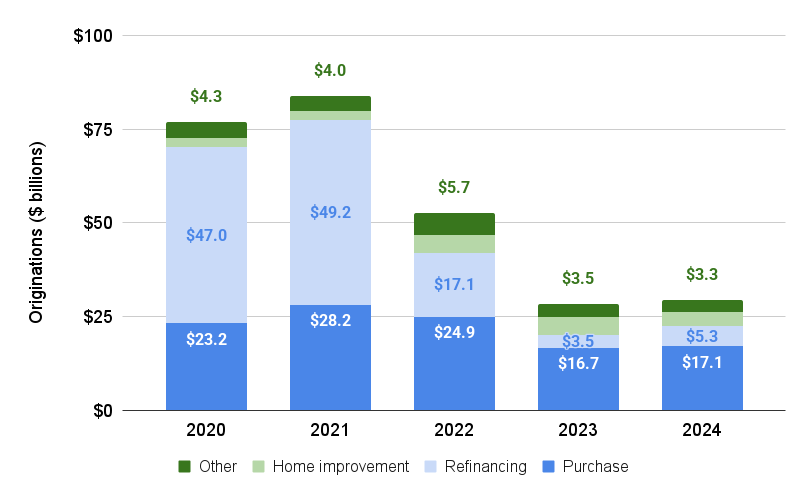

Bank of America mortgage originations, 2020-2024

Bank of America was the nation’s fifth-largest mortgage lender last year by dollar volume, with $29.5 billion in originations, according to an analysis of HMDA data by iEmergent.

Since the end of the pandemic-era refinancing boom fueled by low interest rates, most of the bank’s mortgage business has been with homebuyers, with $17.1 billion in purchase loans funded in 2024.

Regulatory rollback

Vought and his top deputy at OMB, Dan Bishop, are leading the Trump administration’s efforts to downsize the CFPB, with Vought serving a dual role as the bureau’s acting director.

The Trump administration, which is seeking to cut 90 percent of the CFPB’s workforce, has put about 20 active enforcement cases on hold and sought to vacate a number of settlements that the bureau reached under the Biden administration.

The acting director of the CFPB’s enforcement division, Cara Petersen, resigned on June 10, saying in a farewell email that “the bureau’s current leadership has no intention to enforce the law in any meaningful way.”

Two days later, U.S. District Judge Franklin Valderrama declined the CFPB’s motion to vacate a settlement it reached last year in a fair lending case involving Chicago mortgage broker Townstone Financial, saying that doing so “would erode public confidence in the finality of judgments.”

Russell Vought

Vought had claimed that an internal review of the case determined that the CFPB “abused its power” in pursuing the case against Townstone in order to “further the goal of mandating DEI in lending.”

Consumer groups that defended the Townstone settlement in court called the CFPB’s request to vacate it “unprecedented,” and argued that granting it would establish a “dangerous and destabilizing precedent.”

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter