Home-sale prices dipped in 11 metros as buyers show caution

As of April 20, home-sale prices fell across 11 U.S. metro areas, marking the first time this many markets have seen year-over-year declines since September 2023, data released Thursday by Redfin found.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

As of April 20, home-sale prices fell across 11 U.S. metro areas, marking the first time this many markets have seen year-over-year declines since September 2023, data released Thursday by Redfin found.

TAKE THE INMAN INTEL SURVEY FOR APRIL

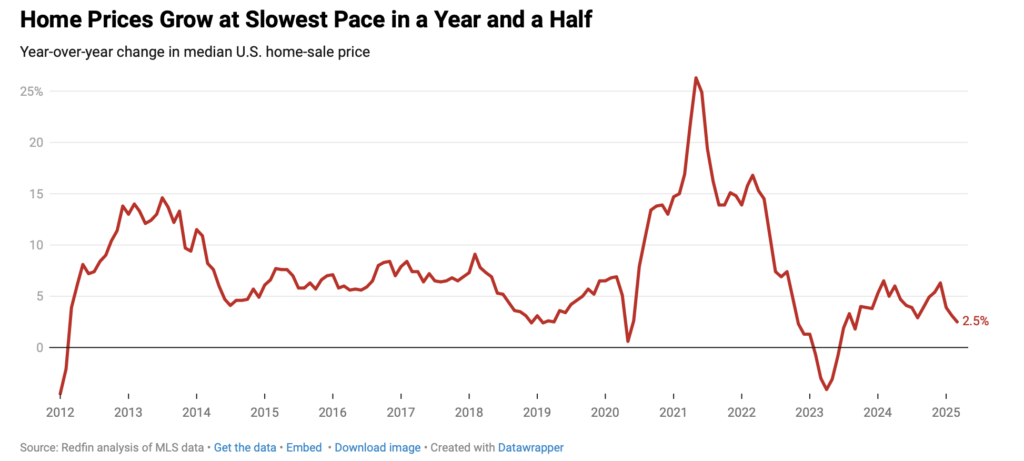

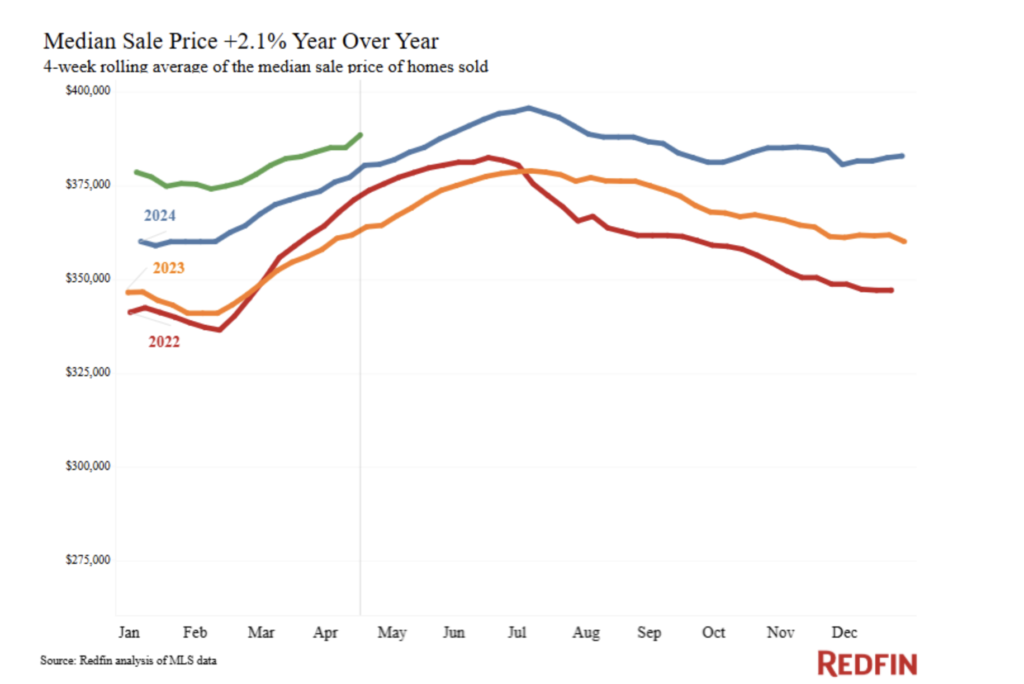

The steepest price drops were seen in San Antonio (-3.7 percent); Oakland, California (-3.5 percent); Jacksonville, Florida (-2.2 percent); and Phoenix (-2.0 percent). Meanwhile, nationwide, the median home-sale price rose just 2.1 percent year-over-year — the slowest pace of growth since July 2023.

Redfin analysis of MLS data

Redfin agents point to ongoing economic uncertainty as a cooling factor. High housing costs, elevated mortgage rates and concerns about a potential recession are making both buyers and sellers more hesitant.

Chen Zhao | Economic Research Lead

“There are always people who need to buy homes or sell homes, no matter what’s going on in the world,” Redfin’s Economic Research Lead Chen Zhao said in a statement. “But with so much uncertainty in the economy, now is a time for those buyers and sellers to be more strategic than ever.”

While prices may be slipping in some metros, that hasn’t exactly translated into faster sales. Homes are sitting on the market for an average of 40 days — up five days compared to a year ago.

And though new listings are up 9.6 percent year over year, much of the current market activity is being driven by sellers, while buyer activity is clearly slowing.

Redfin reports that mortgage-purchase applications are declining, home tours are down, per home touring tech company ShowingTime, and pending home sales have dropped 0.3 percent nationwide.

The biggest slowdowns in pending sales occurred in Miami, Fort Lauderdale and West Palm Beach, Florida; and Las Vegas.

Adding to the strain, mortgage rates continue to climb. The average weekly mortgage rate jumped to 6.83 percent from 6.62 percent the week before, putting the typical U.S. monthly housing payment at $2,848 — $8 short of the all-time high. These rate hikes are also fueled by fears of recession, driven in party by new tariffs and economic instability.

Experts say that in today’s shifting market, strategy is everything.

“My advice to sellers is to price your home fairly for the shifting market; you may need to price lower than your initial instinct to sell quickly and avoid giving concessions,” Zhao said. “On the flip side, buyers should negotiate on price and terms and shop around even more than usual for the best mortgage rates.”