by Richelle Hammiel | Apr 17, 2025 | Industry, News Feed

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

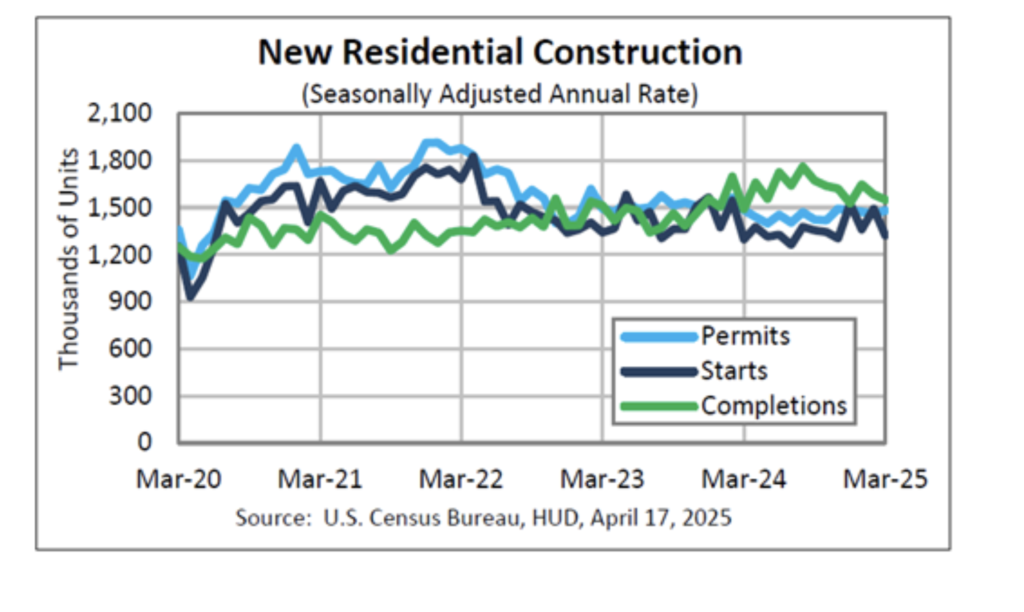

Builders are beginning to pump the brakes on new construction as a mix of affordability pressures and threatened tariffs add fresh uncertainty to the market.

New residential construction improved modestly year over year in March, but the rebound wasn’t nearly as strong as expected, according to new data released Thursday by the U.S. Census Bureau and the Department of Housing and Urban Development (HUD).

TAKE THE INMAN INTEL SURVEY FOR APRIL

In March, privately owned housing starts fell 11.4 percent from February, dropping to a seasonally adjusted annual rate of 1,324,000. Although that figure is 1.9 percent higher than March 2024, it’s not enough to signal a strong recovery. Single-family starts bore the brunt of the pullback, falling 14.2 percent to 940,000 units — the lowest level in six months. Meanwhile, construction of multifamily buildings came in at 371,000.

Tariffs recently implemented or threatened by the Trump administration are already driving up the cost of building materials. According to the National Association of Home Builders (NAHB), 60 percent of builders say their suppliers have increased prices or announced price increases for building material prices due to tariffs.

Builders surveyed by the NAHB say their suppliers have increased prices by 6.3 percent in response to announced, enacted, or expected tariffs, driving up the cost of building a new home by $10,900 on average.

Robert Dietz | National Association of Home Builders

“Policy uncertainty is having a negative impact on home builders, making it difficult for them to accurately price homes and make critical business decisions,” NAHB Chief Economist Robert Dietz said in a statement.

Although builder sentiment inched up slightly in April, from 39 to 40, NAHB Chairman Buddy Hughes said that could reflect a dip in mortgage rates last month that may have helped push some buyers off the fence.

“At the same time, builders have expressed growing uncertainty over market conditions as tariffs have increased price volatility for building materials at a time when the industry continues to grapple with labor shortages and a lack of buildable lots,” Hughes said.

Odeta Kushi | First American Deputy Chief Economist

Builders pulled back more than expected in March amid rising tariff uncertainty, as housing starts slumped well below consensus expectations, First American Deputy Chief Economist Odeta Kushi said in a LinkedIn post.

“Builders face persistent supply-side and affordability challenges, from higher material costs to a shortage of skilled labor,” Kushi added. “Residential building material costs are still more than 40 percent higher than pre-pandemic levels, making construction more expensive.”

The Trump administration imposed 25 percent tariffs on steel and aluminum in March, a 25 percent tariff on autos on April 3, and a 10 percent blanket tariff on imports from most U.S. trading partners on April 5.

Many goods from Mexico and Canada are exempt from the 10 percent baseline tariff under the the United States-Mexico-Canada Agreement (USMCA), including lumber — a decision that the NAHB has called a “major win” for homebuilders. A Biden-era 14.5 percent tariff on Canadian lumber remains in effect.

While country-specific “reciprocal” tariffs of up to 50 percent against dozens of countries are on hold until July 9, imports from China are now subject to 145 percent duties, with additional tariffs of up to 100 percent on specific goods.

New Residential Construction| U.S. Census Bureau

Even so, some aspects of the housing market showed modest resilience. Housing completions dipped just 2.1 percent from February, coming in at a seasonally adjusted annual rate of 1,549,000. Single-family completions inched up by 0.9 percent while more than 503,000 units in multifamily buildings were completed, helping to ease rental supply constraints in some markets.

Looking ahead, the outlook for new construction remains uncertain.

Building permits painted a mixed picture. Overall, permits for privately owned housing units rose 1.6 percent to 1,482,000 in March. However, single-family permits declined 2.0 percent to 978,000, hitting their lowest level in five months, while multifamily permits landed at 445,000.

“The slower pace of single-family permits suggests a reduced rate of groundbreaking in the upcoming months, due to higher inventory levels in key markets and ongoing challenges with costs and affordability,” Kushi noted.

Builder outlooks for the months ahead also showed signs of softening. Optimism about single-family sales over the next six months dropped four points to 43 — the lowest reading since November 2023. While current sales ticked up from 43 to 45, and prospective buyer traffic rose slightly from 24 to 25, both measures remain in negative territory, according to Kushi.

“The gains in measures capturing current conditions are likely due to recent declines in mortgage rates, which could help to coax some buyers off the sidelines,” Kushi said. “However, the worsening outlook for future sales conditions reflects growing builder concerns about costs and affordability.”

This post was originally published on this site

by Richelle Hammiel | Apr 14, 2025 | Industry, News Feed

As of March, the median asking rent dipped slightly year over year to $1,610. That’s just a 0.6 percent decline from the previous year and a slight 0.4 percent increase from February. While those very subtle changes have offered some relief to renters, Redfin economists say that the landscape is shifting, and fast.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Rent prices have been steady over the past 13 months, but that calm may not last much longer. According to a new report from Redfin, mounting economic pressures, including tariffs and slowing construction, could soon put upward pressure on rents.

As of March, the median asking rent dipped slightly year over year to $1,610. That’s just a 0.6 percent decline from the previous year and a slight 0.4 percent increase from February. While those very subtle changes have offered some relief to renters, Redfin economists say that the landscape is shifting — and fast.

A major reason for the shift is the 10 percent blanket tariff on imports, which took effect April 5 under President Trump. While additional “reciprocal” tariffs have been paused, at least temporarily, for most trade partners, China was notably left out of that pause, meaning the supply chain for many goods, including building materials, could still take a hit.

Apartment construction is especially vulnerable as many of the materials needed to build housing, like softwood lumber, are imported. As tariffs drive up those costs, developers may pull back. With fewer new units being built, a supply crunch could drive rents higher — especially in markets where demand remains strong.

However, that’s not the only pressure point. According to Redfin Economics Research Lead Chen Zhao, economic uncertainty is also playing a role.

“Tariffs could also drive up rents by increasing demand,” Zhao said. “People may opt to rent instead of buy homes because the turmoil around tariffs has fueled widespread economic uncertainty. Tariffs have already caused huge swings in the stock market, and they will lead to higher prices for many goods and services, along with increased unemployment.”

That uncertainty is already showing up in renter behavior. In Northern Virginia, Redfin Premier agent Matt Ferris says one of his clients is even thinking about selling their home and renting for a year out of fear of a layoff. Federal employees in the D.C. area, in particular, have been impacted by widespread cuts tied to Elon Musk’s Department of Government Efficiency (DOGE).

At the same time, the cost of homeownership is becoming increasingly out of reach. Redfin reports that the average American now needs to earn over $116,000 annually to afford a median-priced home, nearly double the $64,160 needed to afford a typical apartment.

Some cities are still seeing rents fall, thanks to a backlog of newly built units. In Austin, for example, the median asking rent has dropped 10.7 percent year over year to $1,420. Similar declines were seen in San Diego (-9.7 percent) and in Portland, Oregon, and Minneapolis (-7.8 percent).

Others are trending in the opposite direction. Rents rose the most in Cincinnati (12.1 percent), Providence, Rhode Island (11.4 percent) and Cleveland (10.6 percent). If construction slows and demand rises as expected, more markets could join that list in the coming months.

Email Richelle Hammiel

This post was originally published on this site

by Richelle Hammiel | Apr 11, 2025 | Industry, News Feed

The Amazon founder has sold his luxurious estate in Hunts Point, just outside of Seattle, for $63 million — setting a a new state record, the “Puget Sound Business Journal” reported Thursday. It’s the second time that this particular property has made history.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Jeff Bezos has once again set a real estate record.

The Amazon founder has sold his luxurious estate in Hunts Point, Washington, just outside of Seattle, for $63 million — setting a new state record, the Puget Sound Business Journal reported Thursday. It’s the second time that this particular property has made history.

Bezos originally purchased the 9,420-square-foot waterfront mansion back in 2019 for $37.5 million, which at the time was the most ever paid for a home in the state. That record stood until 2020, when Sunny Singh paid $60 million for a nearby property.

Now, Bezos has reclaimed the title.

More than just a high-priced property, the estate also comes with a notable history. It was once the home to late art collector Barney Ebsworth, and it sits in one of Seattle’s most elite neighborhoods. According to GeekWire, Hunts Point has been home to several other business titans, including former Microsoft CEO Steve Ballmer and Costco co-founder James Sinegal.

The buyer this time around is Detroit-based Cayan Investments, LLC, which now owns the three-bedroom, 4.5-bathroom residence. Nestled on 3.2 acres, the property boasts 300 feet of Lake Washington waterfront and even includes a 2,200-square-foot dock built for boats and seaplanes.

Located at 4053 Hunts Point Road, the home was originally built in 2003 and designed by Seattle architect Jim Olson of Olson Kundig. Olson Kundig’s website describes the residence as an “understated house on the shore of Lake Washington” that “weaves art and nature together, creating a comfortable place to live.”

Even with this major sale, Bezos still holds a significant presence in the Seattle-area real estate market. His portfolio includes two nearby properties in Hunts Point and Medina — a 30,000-square-foot mansion known as the La Haye estate, which he bought in 2010 for $45 million, and an adjacent property he acquired in 1998 for $10 million.

Outside of the Pacific Northwest, Bezos has been busy buying up property in Miami’s exclusive Indian Creek Village — often dubbed the “Billionaire Bunker.” He purchased a $68 million estate there in 2023, followed by a neighboring $79 million mansion. Then, in 2024, he added a third property for $90 million.

The $79 million deal stirred up some legal controversy. The seller — Brazilian toy magnate Leo Kryss — sued real estate firm Douglas Elliman, claiming he wasn’t informed that the buyer was Bezos and accepted an offer $6 million below the asking price.

Email Richelle Hammiel

This post was originally published on this site

by Richelle Hammiel | Apr 10, 2025 | Industry, News Feed

The sale marks the first time the home has changed hands since 2020, when it was purchased for $5.35 million by “Full House” creator Jeff Franklin.

In Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

“When you’re lost out there and you’re all alone, a light is waiting to carry you home,” as the Full House theme song goes — and that light just led a new owner to the iconic Full House home in San Francisco for $6 million.

The famous Victorian home at 1709 Broderick Street, part of the city’s picturesque “Postcard Row,” or “Painted Ladies,” was scooped up by an undisclosed buyer on Monday. The buyer and seller were both represented by Rachel E. Swann of Coldwell Banker Realty.

The sale marks the first time the home has changed hands since 2020, when it was purchased for $5.35 million by Full House creator Jeff Franklin, TMZ reported. The home was listed in June 2024 for $6.5 million, receiving a cut to just under $6 million before landing its final sale.

According to TMZ, the sitcom’s stars left behind a special treat for the new owner — their handprints and signatures in the home’s backyard.

Originally built in 1883 by architect Charles Lewis Henkel, the 3,737-square-foot home underwent a major renovation in 2019 by renowned architect Richard Landry, according to the property’s listing description. The result is a blend of historic charm and modern elegance, complete with white walls, high ceilings and bay windows.

The home features a primary suite with a fireplace and spa-style bathroom, a sleek wet bar, a private fitness room and even a manicured English garden. The home also includes four bedrooms and four baths spread over two spacious floors.

While the interiors of Full House were filmed in a Burbank studio, the exterior of this Pacific Heights home became forever tied to the fictional Tanner family. The sight of it instantly calls to mind the opening credits and nostalgia of the show’s theme song.

Full House, which aired from 1987 to 1995, followed widowed dad Daniel “Danny” Tanner, played by the late Bob Saget, and his household full of love, chaos and unforgettable catchphrases, especially “You got it dude,” delivered by Mary-Kate and Ashley Olsen.

The Netflix reboot Fuller House ran from 2016 to 2020 and reunited much of the original cast, along with that familiar front stoop.

Email Richelle Hammiel

This post was originally published on this site

by Richelle Hammiel | Sep 10, 2024 | Industry, News Feed

Whether it’s refining your business model, mastering new technologies, or discovering strategies to capitalize on the next market surge, Inman Connect New York will prepare you to take bold steps forward. The Next Chapter is about to begin. Be part of it. Join us and thousands of real estate leaders Jan. 22-24, 2025.

Many clients may prioritize emotional connections when hunting for resale homes, but Harrison Polsky of The Polsky Porpino Team at Douglas Elliman takes a deliberate, data-driven approach, focusing his team’s efforts on newly-built properties. This approach is one that few have caught on to, and Polsky uses that to his advantage.

As principal of Douglas Elliman’s leading team in the Dallas-Fort Worth (DFW) metroplex, Polsky leverages his commercial real estate background and residential expertise to provide innovative solutions and top-tier service, fostering long-term client trust.

In a recent conversation with Inman, Polsky shared insights on his sales approach, artificial intelligence (AI), the upcoming election and his plans for Inman Connect Austin in October.

Below is the conversation, edited for brevity and clarity.

Inman: Inman Connect Austin is just over a month away. Do you know what you will be focusing on? Is there anything that you are looking forward to?

Polsky: The topic of my panel is Channeling Market and Economic Forecasts to Attract More Clients. It’s a very broad topic that can go in 20 different directions. A couple of other colleagues of mine will be speaking as well, so I’ll be going into some other panels.

Over half of The Polsky Porpino Team’s sales are from newly constructed homes. Could you share the reasons behind your team’s emphasis on new builds?

I come from a commercial background and work for some of the largest developers in Texas, so I understand that process better than I do resale clients. When I started growing the team, I was looking for agents in that space or people who worked for larger corporations, like Toll Brothers or Lennar, that were salespeople for them because that’s what they understand as well.

There has not been a team that I know of in Texas that has geared towards that one side of the business, and I saw an opportunity there to capitalize on that. I thought, if I can gather a group of individuals who understand that space, I can train them down the road and have a team that holds market share on new construction, which is what we do.

It’s closer to 95 percent of our sales, so of our $140 million that we do a year — next year, we’re slated for $225 million — 95 percent of that is new construction. That’s the service that we offer to builders, which gives us a competitive advantage against other agents because we have so much insight into the market space.

With the influx of people moving within your market leading to a tight inventory supply, is there hope that the market will find balance, and how does that happen?

There are two answers here that need to be understood about balance. DFW is a major metroplex. The data is pooled together in a way that I don’t find to be legitimate, and it skews things in all sorts of different directions.

For example: Dallas proper — Highland Park, Preston Hollow are about 40 minutes from Frisco, 40 minutes from Fort Worth, 30 minutes from South Lake. When we talk about relocation, it’s not all these people relocating to Dallas proper. Yes, Goldman is moving downtown and feeder companies, complementary companies to Goldman are moving near, bringing high-level executives. However, many others are moving up north to Frisco.

When you pull this data together with DFW looped into one data pool, it’s similar to taking Bronx, Queens, Yonkers, New Jersey and Connecticut, and saying that’s one market. There are still a lot of people moving here, but not as many as you think.

The second part of that conversation is the high-end luxury market where most of these people are moving to, whether it’s in Frisco or Dallas proper. For inventory to be released up, rates must drop to the mid- to high-$400,000s. For people to sell their house, they must be able to afford a new one. The problem is that these pockets are so small that most of the people who have been here and bought a house, in say, University Park, for $1.7 million, are not going to sell that house today for $3.4 million, then go buy the same house they just sold. They have to jump up to a different price point, which is going to be $6 million plus.

To do that, you would need to see “the golden handcuff rule.” They’re not only tied into their low interest rate; they have to be able to purchase something else. To loosen inventory up, you have to see places like Frisco thrive — more private schools up north and better public school systems.

AI has been adopted across various industries. Can you detail any AI tools or technologies that you currently employ, and tell me how those tools improve the client experience during your transactions?

I’ve never used AI to interface with my clients to help a transaction. If I’m in the car or on a run and I need to write an email, I’ll say, ‘Hey, ChatGPT this. Copy and paste this email. I need a response and this is the tone I’m looking for,’ which frees up about two hours. That way, when I get to the office, I’m ready to focus on something else.

When I’m trying to articulate to designers, architects or clients what a house is going to look like, there are multiple AI tools where I can say, ‘I need a modern, neoclassical house,’ and they’ll find around 40 different images for inspiration.

Are there any specific policies or proposals from [this year’s presidential] candidates that you believe could influence property values or demand?

We’re real estate people, so this capital gains tax, as proposed by Harris, is disastrous. It’s not going to get passed, so I’m not really worried about it. There have been multiple other California Democrats that have also agreed on that topic, that it would be disastrous to the economy and to entrepreneurs alike.

I don’t believe politics affects anything in our state. We are a pretty red state. We are pretty bullish on real estate, and we’re pretty good [on] taxes here.

Do you anticipate a slowdown or surge in real estate activity leading up to or following the election?

It’s always slow in every election a couple months before. It’s pretty standard after, depending on where you live. That will be geographically specific, but Dallas has always been a really strong economy, no matter who’s in the White House.

Austin seems to have a little bit more ebb and flow depending on that. Austin is heavy tech. Houston depends on that because of Houston’s oil-based economy. Dallas is not so dependent on one industry. If your tech guys are winning and your oil guys are losing, those people are buying and selling.

Have your clients expressed any concerns about the election’s impact on the housing market?

Everyone’s concerned when it comes to an election; that’s why there’s an election. Every four years, people are concerned about one thing or another.

When we talk real estate, we talk data and we talk numbers, and we keep there. Numbers don’t lie, emotions do, so, therefore, that’s what I stay focused on. We work with projections, we look at models, and that’s what we make decisions based on. I don’t make decisions based on which way the wind’s blowing and how I feel today about what someone said on CNBC or CNN or Fox News. I don’t think that’s smart.

Email Richelle Hammiel