Here’s why builders are slamming the brakes on new apartments

According to a new Redfin report, building permits for multifamily units have plunged 27.1 percent from their pandemic-era highs, with new rentals now hitting the market at the slowest pace on record.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Builders in the multifamily housing market are pumping the brakes — and fast.

According to a new Redfin report, building permits for multifamily units have plunged 27.1 percent from their pandemic-era highs, with new rentals now hitting the market at the slowest pace on record.

Sheharyar Bokhari | Redfin Senior Economist Sheharyar Bokhari

“New apartments are being rented out at the slowest speed on record, and builders are pumping the brakes because elevated interest rates are making many projects prohibitively expensive,” Redfin Senior Economist Sheharyar Bokhari said in the report. “At some point in the next year, the slowdown in building will mean that renters have fewer options — potentially leading to an increase in rents.”

In short, building is getting riskier and more expensive.

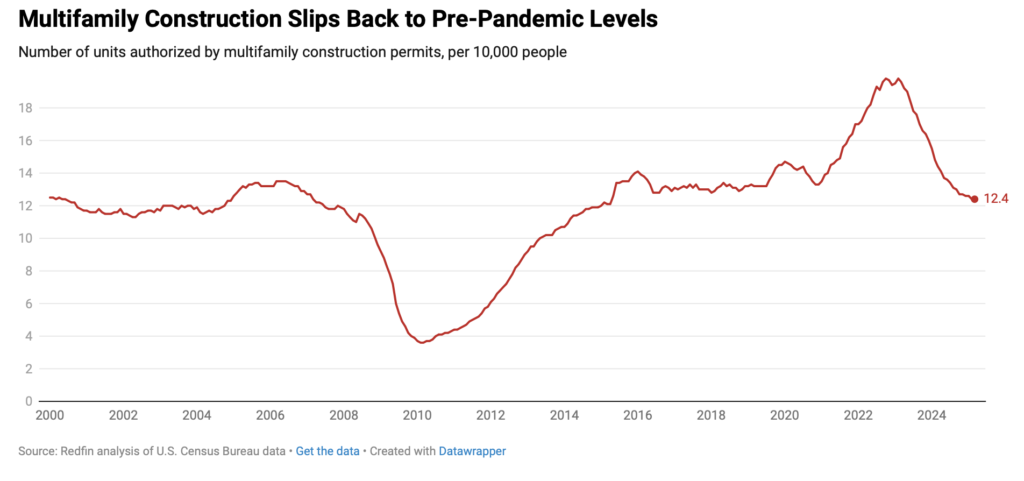

During the height of the pandemic, builders were filing an average of 17 multifamily permits per 10,000 residents. Over the past year, however, the average has fallen to just 12.4 permits per 10,000 people, a 5.5 percent drop from pre-pandemic levels, according to the U.S. Census Bureau’s multifamily housing data.

Redfin analysis of U.S. Census Bureau data

It’s not just interest rates dampening builder enthusiasm. Tariffs imposed under the Trump administration are adding costs to construction materials.

The combined effect of higher borrowing costs, slowing rent growth and steeper material prices have caused builders in many metro areas to pull back. In fact, 63 percent of markets analyzed by Redfin saw a decline in multifamily permitting since the pandemic.

Redfin analysis of U.S. Census Bureau data

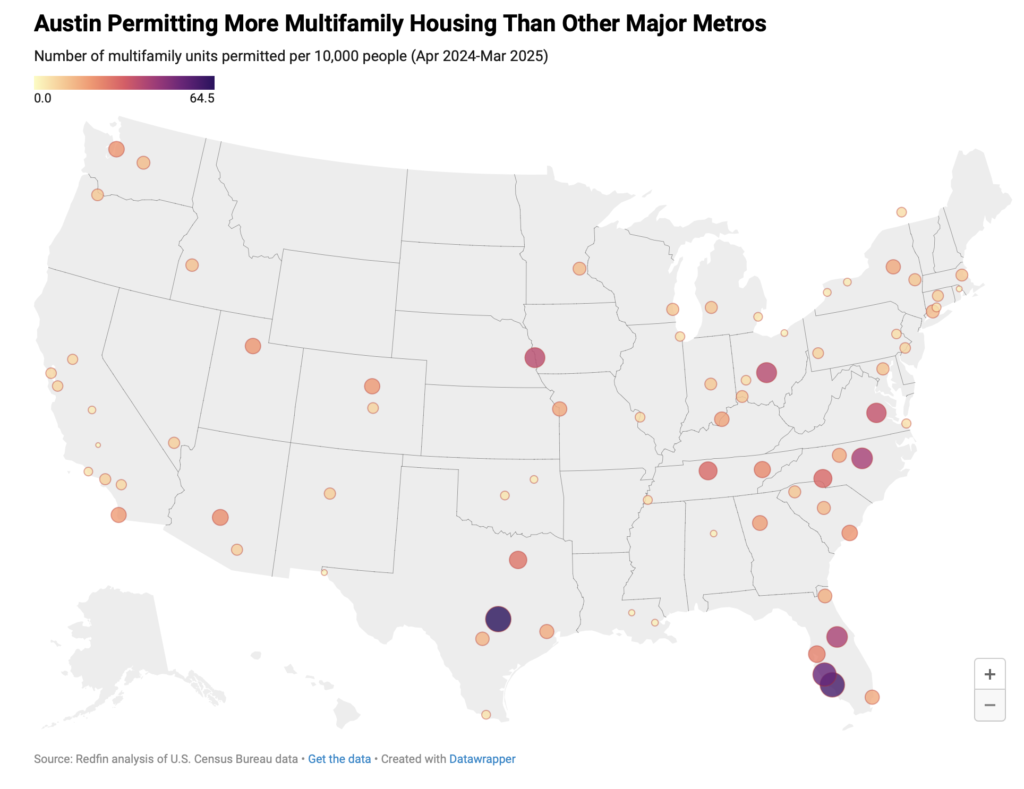

Stockton, California, for instance, saw permitting drop to zero. Colorado Springs, Colorado, fell 82 percent to just 8.6 units per 10,000 people, while Boise City, Idaho, declined 64 percent to 12.6 units.

Still, there are bright spots. A few cities are defying the trend and ramping up construction. Oklahoma City led the way with a 193 percent increase in permits — from just 1.7 units per 10,000 people during the pandemic to 5.1 over the past year. Austin, Texas — where remote work fueled a surge in housing demand and construction following the pandemic — led all major metros with 64.5 units permitted per 10,000 people.

Cape Coral, Florida (59.6); North Port, Florida (53.3); and Raleigh, North Carolina (41.1), also saw significant multifamily growth.

Even so, Redfin warns that today’s slowdown could become tomorrow’s supply crunch. If construction continues to lag, renters may soon find themselves facing fewer options and potentially higher rent prices.