by Marian McPherson | Jul 1, 2025 | Industry, News Feed

California Governor Gavin Newsom has signed the state’s 2025-2026 budget, which offers environmental review exemptions for critical housing and infrastructure projects. Leaders say the exemptions will improve affordability, while environmentalists say it will ruin the state’s ecosystem.

Real estate is changing fast, and so must you. Inman Connect San Diego is where you turn uncertainty into strategy — with real talk, real tools and the connections that matter. If you’re serious about staying ahead of the game, this is where you need to be. Register now!

Amid a worsening housing affordability and homelessness crisis, California legislators have made a drastic move to bolster inventory levels throughout the state.

On Monday, Governor Gavin Newsom announced that he’d signed Assembly Bill 130 and Senate Bill 131, both of which include sweeping reforms to California’s building permit and new residential building standards systems, alongside greater oversight of city and county homeless shelters and an increase to the Renters Tax Credit.

TAKE THE INMAN INTEL INDEX SURVEY FOR JUNE

However, the most consequential change within AB 130 and SB 131 is the streamlining of the state’s 55-year-old environmental protection law, California Environmental Quality Act (CEQA).

Although originally limited to government projects, CEQA’s strict environmental reviews expanded throughout the decades to include private housing projects. Legislators on both sides of the aisle said the reviews, which are meant to identify and mitigate risks to air, water quality, biodiversity, habitats and ecosystems, had become too cumbersome.

The CEQA reform offers exemptions to high-density projects not on environmentally sensitive or hazardous sites, and critical housing and infrastructure projects, including infill housing, high-speed rail facilities, utilities, broadband, community-serving facilities, like child care centers, and farmworker housing. The reform also opens the door for municipalities to rezone commercial projects, like malls and office buildings, into multifamily housing with more ease.

“This isn’t just a budget. This is a budget that builds. It proves what’s possible when we govern with urgency, with clarity, and with a belief in abundance over scarcity,” Newsom said in a prepared statement on Monday. “In addition to the legislature, I thank the many housing, labor and environmental leaders who heeded my call and came together around a common goal — to build more housing, faster and create strong affordable pathways for every Californian.”

“Today’s bill is a game changer, which will be felt for generations to come,” he added.

Both bills received bipartisan support, with AB 130 receiving a unanimous vote from the Assembly and a 28-5 vote from the Senate. SB 131 received similar support, passing the Assembly 50-3 and the Senate 33-1.

Senator Scott Weiner, who represents Senate District 11 in San Francisco, said the bills’ passage will enable the state to “move the needle on affordability.”

“It isn’t easy to make changes this big, but Californians are demanding an affordable future, and it’s our job to deliver for them no matter what,” he said in a written statement. “I’m incredibly proud of the work Governor Newsom, Assemblymember Wicks, Speaker Rivas, and my friend and partner Pro Tem McGuire did to push this bold package across the finish line and set us on a path to build again in California.”

Although legislators and several housing groups, such as the United Brotherhood of Carpenters, MidPen Housing and California YIMBY, are praising CEQA’s reform, environmentalists are ringing the alarm bell, saying the exemptions could yield potentially deadly consequences.

“It blows a hole in our efforts to protect habitat,” environmental lobbyist Kim Delfino told The New York Times on Monday. “Make no mistake, this will be devastating.”

Political experts said California’s decision could set the stage for more states, especially those with Democratic leaders looking to woo voters with the promise of more affordable housing, to relax environmental reviews and permitting laws.

“This has created a different political environment,” Public Policy Institute of California survey director Mark Baldassare told the Times. “Voters have been telling us in our polling for quite a while that the cost of housing is a big problem, but maybe for the elected officials, the election itself was a wake-up call.”

Email Marian McPherson

by Marian McPherson | Jun 13, 2025 | Industry, News Feed

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

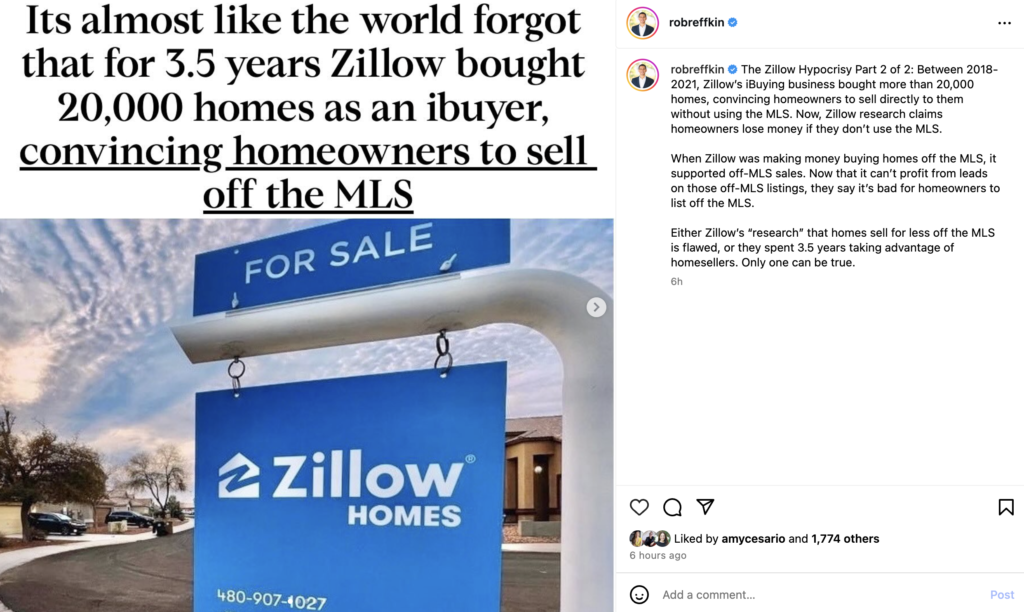

Compass CEO Robert Reffkin is ending the week the same way he began it: lambasting Zillow for its “hypocrisy” regarding off-market listings.

“Between 2018-2021, Zillow’s iBuying business bought more than 20,000 homes, convincing homeowners to sell directly to them without using the [multiple listing service],” the Instagram post read. “Now, Zillow research claims homeowners lose money if they don’t use the MLS.”

“When Zillow was making money buying homes off the MLS, it supported off-MLS sales,” he added. “Now that it can’t profit from leads on those off-MLS listings, they say it’s bad for homeowners to list off the MLS. Either Zillow’s ‘research’ that homes sell for less off the MLS is flawed, or they spent 3.5 years taking advantage of homesellers. Only one can be true.”

The post garnered 1,775 likes and 106 comments from brokers, 105 of whom supported Reffkin’s view on Zillow’s business model.

“So glad you are pushing against Zillow! They can’t survive without our inventory,” read one comment.

“Zillow took advantage of sellers and lost money. Now they’re back to trying to protect their revenue via control of others’ access to listings,” read another comment. “Sounds about right for corporate greed.”

READ INMAN’S ZILLOW LISTING BAN FAQ

A sole commenter backed Zillow and its now-defunct Zillow Offers segment, saying it’s unfair to compare iBuying to private listing networks. All homebuyers, they said, had access to Zillow Offers listings after Zillow purchased the home, remodeled and repaired it, and placed it back on the open market. Meanwhile, listings circulated within private listing networks usually never make it to the wider public, unless the homeseller changes their mind.

“Everyone has access to Zillow as opposed to Compass, which has a database only for their agents and homebuyers so they can double-end deals,” the comment read. “[That] makes shareholders happy while disenfranchising agents and customers that don’t want to work for Compass.”

A company spokesperson pushed back on that response, saying Compass doesn’t agree with those saying the company “is just doing this to double-end more deals.”

“In the world of signed buyer representation agreements, Compass is going to make the exact same amount of money if a buyer buys a private exclusive or a listing from a different brokerage,” they said. “The agreement says they have six to nine months. It doesn’t matter. It seems like ‘organized real estate’ is using the same arguments for control that worked before the settlement required buyer rep agreements last Aug. 17 and didn’t realize that the world changed to a point where the argument no longer makes sense.”

Reffkin’s Instagram post on Friday, June 13.

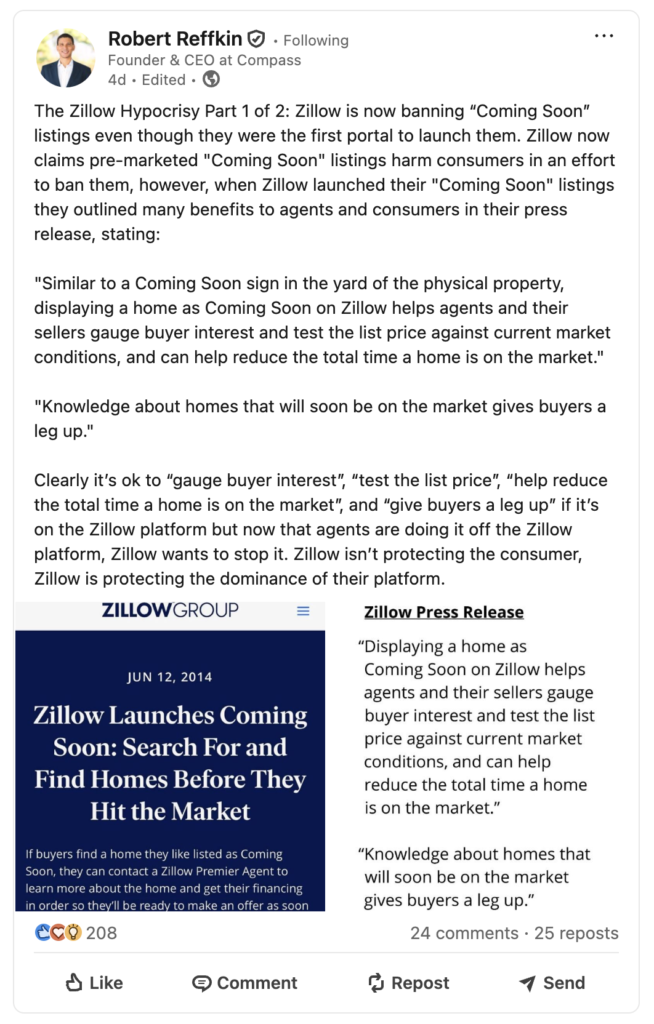

Reffkin’s Instagram post follows a post on LinkedIn from Monday, where the CEO attacked Zillow’s 2014 Coming Soon search function, which enabled homebuyers to view “coming soon” listings and contact a Zillow Premier Agent for more information on that listing.

Reffkin said Zillow is planning to ban “coming soon” listings — which Zillow has told Inman is not true — and said the move is hypocritical.

“Zillow now claims pre-marketed ‘Coming Soon’ listings harm consumers in an effort to ban them; however, when Zillow launched their ‘Coming Soon’ listings, they outlined many benefits to agents and consumers in their press release, stating: ‘Similar to a Coming Soon sign in the yard of the physical property, displaying a home as Coming Soon on Zillow helps agents and their sellers gauge buyer interest and test the list price against current market conditions, and can help reduce the total time a home is on the market. Knowledge about homes that will soon be on the market gives buyers a leg up,” the post read.

“Clearly it’s ok to ‘gauge buyer interest,’ ‘test the list price,’ ‘help reduce the total time a home is on the market’ and ‘give buyers a leg up’ if it’s on the Zillow platform but now that agents are doing it off the Zillow platform, Zillow wants to stop it,” it added. “Zillow isn’t protecting the consumer, Zillow is protecting the dominance of their platform.”

The LinkedIn post garnered a similar reaction to Reffkin’s Instagram post, with 25 commenters praising the CEO’s push against Zillow ahead of the portal’s listing ban, which will impact thousands of Compass homesellers and listing agents using the brokerage’s three-phase marketing strategy, which involves launching listings as private exclusives, then “coming soon” properties and, ultimately, on public listing portals.

“Such a revealing contrast, when it served them, Zillow praised ‘Coming Soon’ listings as innovative,” a commenter said. “Now that agents use it independently, it’s suddenly harmful? This isn’t about consumer protection, it’s about platform control.”

Reffkin’s Instagram post on Monday, June 9.

Reffkin’s posts come as Zillow finishes the second week of sending non-compliance notices for listings that aren’t added to the multiple listing service (MLS) within 24 hours of being publicly marketed.

Zillow Group has taken a “three-strikes” approach in which brokers will receive warnings for their first two non-compliant listings before having their third non-compliant listing banned from Zillow, Trulia and StreetEasy on June 30.

The ban doesn’t impact “coming soon,” office exclusives or Delayed Marketing Exempt Listings (DMEL) as long as brokers are adhering to NAR’s guidance for each listing status, Inman’s ban FAQ explained. For sale by owner (FSBO) listings and rental listings won’t be impacted by the ban. New construction listings sold by the builder are also exempt, unless they are listed with a broker under an exclusive listing agreement, in which case, they’ll also be held to the new standards.

Zillow declined to comment for this article.

Email Marian McPherson

by Marian McPherson | Jun 13, 2025 | Industry, News Feed

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

It’s been a week since the National Association of Realtors changed its Realtor Code of Ethics’ Standard of Practice 10-5, which no longer includes the terms “hate speech, epithets, or slurs” and now only applies to “Realtors’ actions in their capacity as real estate professionals.”

Although NAR has defended the changes — with NAR director Matt Difanis saying the adjustments don’t impact “the spirit” of the policy — several affinity group and inclusion leaders say the shift on which activities the policy applies will complicate brokerage leaders’ ability to hold their agents accountable for what they say or do outside of the office.

Gary Acosta

“I’m just gonna speak openly with you, and this is my own sort of speculation, to a certain degree, that NAR is doing the types of things that many corporations are doing right now,” the National Association of Hispanic Real Estate Professionals (NAHREP) Co-founder and CEO Gary Acosta said.

“They’re looking for ways to reduce potential liability, and I think they’re looking for circumstances where they may be viewed as maybe prioritizing one community over the other too much,” he added. “Whether it’s true or not, I do think that’s what all companies are sort of dealing with right now.”

The NAHREP CEO’s speculation appears to ring true, with NAR Professional Standards Committee Chair Todd Beckstrom saying on the day of the vote that the policy changes not only “provide much needed clarity to members,” but also “reduce risk to state and local associations and their volunteer leadership who administer and enforce Article 10.”

Even if the policy changes mitigate risk for state and local associations, Acosta said there could be an opposite impact for brokerage leaders looking to uphold NAR or their company code of ethics.

“I think what NAR is doing is pushing that responsibility from themselves to the individual employers who are members of their organization,” he said. “It becomes up to the local real estate brokerage and the real estate offices out there to ensure that their employees aren’t engaging in behavior that would expose the company to liability or a negative image in those communities. I think that’s the net result of the policy change.”

“I’m an employer, and if I have an employee who is engaging in hate speech, or, let’s just say, racist behavior online or somewhere else, does that give me the right to terminate that employee if it violates some code of conduct that we have within our company? I think it does,” he added. “Also, as the head of an organization, can I deny someone engaging in that kind of behavior membership in our organization? I think we can.”

Brooks Glenn | Credit: LinkedIn

Windermere Director of Inclusion and Community Engagement Brooks Glenn said he agrees with Acosta that brokerages will have a bigger responsibility in holding Realtors accountable for violations of 10-5. However, he’s concerned with brokers’ ability to manage ethics complaints and make decisions in their offices regarding discriminatory behavior, now that the policy only applies to Realtors “in their capacity as real estate professionals.”

“That limitation is an issue. It’s an issue because Realtors are public-facing professionals, and our influence extends well beyond contracts and closings,” he said. “So if a Realtor, for example, posts hate speech on social media or behaves in a discriminatory way in public, yet outside of a real estate transaction, it’s no longer considered a violation. I think that will create space for harmful behavior that could impact the communities we say we want to serve.”

In light of the policy change, Glenn said brokerages will have to strengthen their code of ethics to address all forms of discrimination and bias, which includes blatant hate speech to more nuanced situations, like microaggressions. Alongside stronger codes of ethics, Glenn also said brokerages will need to invest in diversity, equity, and inclusion training that helps agents and team members understand how to navigate racial, gender, sexual, etc. differences with respect.

“At Windermere, we’ve reaffirmed our commitment to diversity, equity, and inclusion in the space of real estate, we’ve looked at the historical harms, and what’s our role in correcting those harms,” he said. “The term DEI has been politicized, hence why my title is the director of inclusion and community engagement.”

“Community engagement is the heart of all of this — how can we position ourselves to provide access to homeownership for all? Again, this change has the potential to hurt this goal, which honestly, we should all have,” he added. “It makes us focus solely on the result, the transaction, and not the everyday abuse that happens and erodes community trust in us.”

LGBTQ+ Real Estate Alliance President Justin Ziegler said his members are worried about the change, especially given the Alliance’s latest annual report that revealed a concerning rise in anti-LGBTQ+ sentiments among agents.

“I can’t speak for everyone, but I can tell that a lot of our members feel that this is going to ultimately water down the code of ethics,” he said. “I have heard absolutely nothing that [the change] would, anyway, impede people from continuing to file a complaint. But we do worry that it will reduce Realtor organizations’ ability to ultimately rule on these types of complaints.”

Ziegler echoed Glenn’s concerns about the attempted separation between a Realtor’s actions inside and outside of a transaction or real estate activity, saying that Realtors often leverage their non-real-estate interests to build their businesses. In an attempt to make things more clear-cut, he said, NAR may have made the process of upholding Article 10 more difficult.

“Think about your typical real estate agent, unless they’re a secret agent, they probably have the fact that they are a Realtor all over their Instagram profile, all over the header on their Facebook,” he said. “And so when you think about that, if the Realtor or brokerage header remains constant at the top of the page and they’re spouting really hateful things in their posts, can you say that there is a separation between what they do in business and everyday life? I don’t think so.”

For brokers who are concerned about hiring discriminatory agents, and for agents who are concerned about hitching their license to a discriminatory broker, Ziegler said the best line of defense is having open, honest, and direct conversations about fair housing and the obligation to maintain a non-discriminatory culture.

“When you are interviewing where you’re going to ultimately hold your license, I think that it’s important to ask very hard-hitting questions about what that broker does to represent you, how they’re taking care of you, and how they run their business,” he said. “Ask them, outright, that if you were discriminated against, would they be willing to file an ethics complaint on your behalf, if you were worried about retaliation. Their answer will let you know if you’re in a safe working environment.”

“On the other side of this, for broker owners, it’s their company, right? They have built a reputation in their community, and it’s critically important to them that every agent represents that broker-owner, the company and the brand well,” he added. “If you’re a broker-owner interviewing agents, you really need to articulate the values of that company and the repercussions if you don’t uphold those values.”

All three leaders said the consequences of the policy change have yet to be seen, and it’s a toss-up on whether NAR’s intended outcome will be what happens. In the meantime, they said brokers and agents should be focused on sharpening their ethical compass and doing the work of clearly defining how an equitable and inclusive industry behaves.

“Discrimination in all forms is still illegal. I think the desire to create a meritocracy in the housing industry and other industries is something everybody shares,” Acosta said. “And I think everybody strives towards creating equality of opportunity for ourselves and the communities we serve.”

“I think this environment — the debates about DEI and NAR’s policy change — will force us to define our goals for equity and inclusion a little bit better,” he added. “And I’m not sure that that’s entirely bad.”

Email Marian McPherson

by Marian McPherson | Jun 12, 2025 | Industry, News Feed

The Senate confirmed Department of Housing and Urban Development Chief of Staff Andrew Hughes as the department’s deputy secretary. Hughes also worked under former Secretary Ben Carson.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Four months after securing his confirmation, Department of Housing and Urban Development Secretary Scott Turner finally has a deputy.

The Senate confirmed Andrew Hughes on Wednesday in a vote of 51-43, elevating the two-time HUD chief of staff to chief operating officer. In his role, Hughes will guide the department’s day-to-day operations.

Scott Turner | Credit: America First Policy Institute

“Andrew Hughes is a servant leader and is the right person, at the right time, for this assignment to carry out HUD’s mission,” Turner said in a prepared statement. “I had the pleasure of serving alongside him during the first Trump administration and witnessed firsthand his leadership, wisdom, and love for this country.”

“We share a clear vision for HUD’s future, and it is truly a blessing to have him in this role,” he added. “He will serve the American people well.”

Before joining HUD under former Secretary Ben Carson, Hughes had no political experience. The now-deputy worked as a special projects coordinator for the University of Texas System and a part-time Uber driver. At UT, Hughes oversaw the university’s social media and websites, compiled press releases, planned university events, and researched funding opportunities and higher education legislation.

Hughes joined Carson’s 2016 presidential campaign team and transitioned to helping the Trump campaign when Carson dropped out of the presidential race. His work with Carson and Trump paid off, with Carson tapping Hughes to become his department liaison after taking the helm at HUD in 2017. After the end of President Trump’s first term, Hughes followed Carson to the conservative think tank, the American Cornerstone Institute.

Former HUD Secretary Ben Carson, Senate Banking Committee Chairman Senator Tim Scott and the Mortgage Bankers Association all backed Hughes’s confirmation, with MBA President and CEO Bob Broeksmit noting that the deputy’s prior experience “gives him a unique perspective on ways to improve HUD’s operations, including its programs to support affordable homeownership and rental housing opportunities.”

Andrew Hughes | Credit: HUD

“MBA congratulates Andrew Hughes on his confirmation to serve as HUD Deputy Secretary,” Broeksmit said in a prepared statement on Wednesday. “We look forward to continuing our important work with him, Secretary Turner, and HUD staff on policies and initiatives that lower single-family and multifamily financing costs and increase homeownership and rental housing opportunities for all Americans.”

Hughes thanked the Senate for confirming him, saying, “Serving at HUD is more than a job — it’s a calling.”

“I’m humbled to help lead an agency that expands opportunity for all communities — rural, tribal, and urban,” he added in a prepared statement. “Together, under the leadership of President Trump and Secretary Turner, we’re focused on ensuring more Americans can achieve not just housing, but the stability, self-sufficiency, and upward mobility that define the American Dream.”

Although Hughes fills a crucial spot, the Partnership for Public Service’s political appointee tracker reveals there are still several key roles at HUD that are vacant.

The Senate is awaiting nominations for the commissioner of the Federal Housing Administration (FHA), the president of Ginnie Mae, the HUD senior and general counsel and the HUD assistant secretary for public affairs. Hughes is still listed as HUD’s chief of staff, and it’s unknown whether he’ll take on a dual role or appoint a replacement.

Email Marian McPherson

by Marian McPherson | Jun 12, 2025 | Industry, News Feed

The Zillow-owned portal appeared to shed listings Wednesday after the Fairness in Apartment Rental Expenses Act became law, but a spokesperson insisted daily fluctuations are common.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

In the hours after the enforcement of New York City’s broker fee bill, the Fairness in Apartment Rental Expenses (FARE) Act, StreetEasy lost more than 1,000 rental listings.

The Real Deal began tracking StreetEasy’s NYC rental listing count at 3 p.m. EST on Tuesday. That afternoon, the Zillow-owned site boasted 13,383 listings, 9,136 of which were already no-fee. By 1:30 p.m. EST on Wednesday, when FARE, which requires property owners to cover broker fees for the agents they hire to list a unit, went into effect, the rental listing count had dropped to 12,160.

A StreetEasy spokesperson told TRD the listing drop shouldn’t be attributed to FARE, as this type of fluctuation is typical in New York City, where thousands of renters are signing leases in a given day.

In a conversation with Inman, the spokesperson added additional insight, saying that a day — or even a few weeks — of rental listing declines wouldn’t signal a FARE-induced market collapse, especially since most NYC rentals are already no-fee and renters are becoming more active in the summer. Some of the drop may also be attributed to property owners and brokers temporarily pulling listings to get in compliance with FARE, the spokesperson added.

The portal said it will continue to carefully track rental trends, and said early data shows that FARE hasn’t led to an extreme rise in rents.

“The average annual growth in asking rents of the properties that dropped a broker fee was 5.3 percent in April, only slightly above the 4.6 percent growth for the rest of the market in which broker fees remained in place,” a StreetEasy report read. “The FARE Act is unlikely to alter how property managers set asking rents based on market demand. Asking rents are primarily driven by market conditions, rather than solely by property managers’ costs.”

As of Thursday at 12 pm ET, the NYC rental listing count on the site has remained steady, with 12,175 listings.

Due to FARE, StreetEasy has removed the filter for no-fee apartments and added an alert that reads, “Under NYC law, you can’t be charged a broker fee if you didn’t hire a broker.”

Although FARE is officially NYC law, the fight over the controversial bill is far from over.

The Real Estate Board of New York’s (REBNY) lawsuit against the City to stop FARE’s enforcement is still in play, despite Southern District of New York judge Ronnie Abrams denying the association’s preliminary injunction request on Wednesday.

REBNY’s suit argues that FARE is “constitutionally defective” and preempted by New York state laws that protect commercial free speech and already regulate compensation for real estate brokers and salespeople. The lawsuit also claims the FARE Act violates the Contracts Clause of the U.S. Constitution since brokers and landlords can’t execute existing listing agreements that require brokers to negotiate and receive compensation from tenants.

“New Yorkers will soon realize the negative impacts of the FARE Act when listings become scarce and rents rise,” REBNY President Jim Whelan said on Wednesday. “We will continue to litigate this case as well as explore our avenues for appeal.”

As REBNY revs up for the next stage of its suit, Councilmember Chi Ossé, who authored FARE, used his X and Instagram accounts to remind renters about the bill’s enforcement and urge them to report any property owners who are violating FARE by recasting broker fees as “management fees” to the City’s Consumer Protection Law team.

“Know your rights so landlords + brokers can’t scam you – SPREAD THE WORD,” Ossé said.

Email Marian McPherson