by Richelle Hammiel | Jun 12, 2025 | Industry, News Feed

Imelda Collins launched the “Win a House Near Sligo” raffle to give one lucky winner the keys to her “fairytale Irish country home” in County Leitrim, Ireland. Over 150,000 tickets were sold, and in the end, Kathleen Spangler of Chicago emerged as the winner.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

In the midst of an unpredictable housing market, where many are unsure whether to jump in or hold back, thousands took a chance on an unconventional path to homeownership. And for one woman, that gamble paid off.

Imelda Collins launched the “Win a House Near Sligo” raffle to give one lucky winner the keys to her “fairytale Irish country home” in County Leitrim, Ireland. Over 150,000 tickets were sold, and in the end, Kathleen Spangler emerged as the winner.

Spangler now owns the property mortgage- and rent-free, all thanks to that £5 ticket.

“The current housing crisis in Ireland makes it extremely difficult to buy or rent, so this is an incredible opportunity to own your own home,” Collins explained on UK-based raffle site Raffall. “If you win my home, you will be MORTGAGE AND RENT FREE!, and I will pay your legal fees and stamp duty!”

Following her May 22 win, Spangler responded on Raffall, “If this is indeed real, I absolutely accept.”

Inman has reached out to Spangler for further comment but did not immediately receive a response.

Collins noted that she plans to donate a portion of the raffle’s proceeds to the Irish Society for the Prevention of Cruelty to Animals (ISPCA), a charity that she says is close to her heart. As for the rest, Raffall will take 10 percent — Collins will receive the remainder, minus affiliate commissions and taxes — after covering advertising and marketing expenses related to the raffle.

The prize home is a newly renovated and redecorated 1.75-acre property just 15 minutes away from Sligo. According to Collins, “a wonderful feature of the property is that it benefits from a south-facing position, ensuring sunshine from sunrise to sunset.”

Collins originally purchased the home in 2022 for €133,000 and estimates that it is now worth around €300,000, thanks to significant upgrades.

The home was renovated in 2022, with new insulation, rewiring, replumbing, new carpentry, modern appliances and high-quality furnishings, which will all belong to Spangler with the exception of one “sentimental furniture piece” and some personal wall art.

The interior of the house includes a spacious living and dining area, kitchen, bathroom and two double bedrooms. The exterior features front and back gardens, a garden shed, a large patio with countryside views, and gated access to an open meadow.

While Collins has not yet commented further on the raffle’s outcome, she simply told Inman, “For the moment, we are letting it all sink in.”

Email Richelle Hammiel

by Richelle Hammiel | Jun 12, 2025 | Industry, News Feed

Since the NAR commission suit settlement, buyer agents have faced new rules, new documents and a new normal. This month, Inman drills down on Today’s Buyers Agent with the fresh marketing strategies, skills and tools buyer agents are using to prosper in changing times.

Purchasing a luxury home often comes with a hefty price tag, but in some U.S. metros, high-end living can still be surprisingly affordable. Location, design and luxury amenities can certainly drive up costs, but in seven major U.S. metros, buyers can still find luxury homes priced under $1 million.

According to a new report from Redfin, Detroit, Michigan; Cleveland, Ohio; Pittsburgh, Pennsylvania; Indianapolis, Indiana; St. Louis, Missouri; Cincinnati, Ohio; and San Antonio, Texas, currently offer this level of affordability.

While that’s encouraging news for buyers looking for upscale homes at lower price points, the list has shrunk drastically. Five years ago, 30 metros offered similar opportunities. Between 2013 and 2017, that number was even higher at 35. But by 2020, it had dropped to 30, and today, only seven remain in that category.

Sheharyar Bokhari | Redfin Senior Economist

“The Rust Belt’s relative affordability has preserved opportunities for luxury buyers that have all but disappeared in much of the country,” Redfin Senior Economist Sheharyar Bokhari said in Redfin’s report. “These metros haven’t seen as much explosive investor demand or speculative buying, which has helped keep prices grounded.

“Buyers can get historic charm, large lots, and upscale finishes — often in walkable, tree-lined neighborhoods — for a small fraction of what a similar home would cost in cities like San Francisco or New York.”

1. Detroit, Michigan

Canva: Detroit, Michigan

Detroit has undergone a major transformation in recent years. With revitalized neighborhoods and an influx of development, the city’s housing market is catching up, though prices are still low compared to coastal markets.

As of 2025, the median luxury home sale price in Detroit is $753,851, a $220,294 increase from 2020. Going back a full decade, the price has surged 81.2 percent between 2015 and 2025.

2. Cleveland, Ohio

Canva: Cleveland, Ohio

With a mix of classic architecture and access to a steady economy, Cleveland appeals to buyers seeking character without big-city price tags.

Cleveland’s median luxury home sale price currently sits at $757,046. That’s up from $531,461 in 2020 and $476,170 in 2015, a 59 percent increase over the past 10 years.

3. Pittsburgh, Pennsylvania

Canva: Pittsburgh, Pennsylvania

Pittsburgh has reinvented itself from a steel town to a center for healthcare, tech and education. That revitalization has extended to its housing market, where buyers still find high-end homes at more approachable prices.

The median luxury home price in Pittsburgh is $846,715 in 2025. That a 53.2 percent increase from $552,799 in 2015, and it’s up from 2020’s median price of $618,837.

4. Indianapolis, Indiana

Canva: Indianapolis, Indiana

Indianapolis’ affordability and quality of life make it a standout. The city offers strong schools and family-friendly neighborhoods at prices that remain relatively accessible.

In 2025, the metro’s median luxury home price is $914,276, up from $616,613 in 2020. In 2015, that number was $553,161, reflecting a 65.3 percent jump over the decade.

5. St. Louis, Missouri

Canva: St. Louis, Missouri

St. Louis offers Midwestern charm, a growing cultural scene and historic neighborhoods that continue to attract buyers.

Luxury homes here are priced at a median of $914,453 in 2025, nearly identical to Indianapolis. That’s up from $677,578 in 2020 and $602,076 in 2015, which is a more modest but still substantial 51.9 percent growth over the 10-year span.

6. Cincinnati, Ohio

Canva: Cincinnati, Ohio

Cincinnati has become a standout for luxury buyers in search of large homes and tree-lined streets at lower price points. Its strong job market and downtown area add to its appeal.

In 2025, the city’s median luxury home price is $931,145, the second highest on the list. That’s a 70.2 percent increase from 2015’s $547,238 and up from $600,709 just five years ago.

7. San Antonio, Texas

Canva: San Antonio, Texas

San Antonio is known for its rich culture and booming population. While it’s the priciest of the seven metros on this list, it still offers luxury homes under the million-dollar mark.

The median luxury sale price in 2025 is $957,854, up from $656,438 in 2020 and $567,799 in 2015. That’s a 68.7 percent increase over the past 10 years.

For perspective, the national median luxury home price in 2025 is $1,348,065 — up from $797,903 in 2020 and $717,004 in 2015. That’s an 88 percent jump over the past decade, highlighting just how rare these seven relatively affordable metros have become in today’s high-priced market.

Email Richelle Hammiel

by Richelle Hammiel | Jun 9, 2025 | Industry, News Feed

A wave of “Altadena Not for Sale” signs dot the yards of fire-scarred properties as a plea to preserve the communities that have been lost in January’s Eaton fire. Behind the signs, a different reality is unfolding — Altadena is for sale, and developers are lining up to buy in, the “Los Angeles Times” reported Thursday.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

A wave of “Altadena Not for Sale” signs dot the yards of fire-scarred properties as a plea to preserve the communities that have been lost in January’s Eaton fire. Behind the signs, a different reality is unfolding — Altadena is for sale, and developers are lining up to buy in, the Los Angeles Times reported Thursday.

So far, around 145 properties have been sold, 100 are currently listed and dozens are in escrow. By comparison, the Palisades, another fire-affected area, has seen fewer than 60 sales, with about 180 lots still lingering on the market.

Real estate records show that developers are behind many of the Altadena purchases, with firms Black Lion Properties, Iron Rings Altadena and Sheng Feng acquiring multiple lots. Roughly half of the lots have gone to individual buyers, while the other half were purchased in bulk by these development firms.

Six thousand homes were destroyed in the Eaton fire, leaving a long road to recovery, but sales activity has picked up each month. Homes are selling faster, too.

In the first four months of the year, the median Altadena lot spent just 19 days on the market, compared to 35 days during the same period last year, a report from Redfin shows. Prices range widely, from $330,000 to $1.86 million, with most selling between $500,000 and $700,000. Most buyers are now paying close to asking price.

For many longtime residents, the emotional toll is deep. “In a perfect world, my neighbors and I would all rebuild, and five years from now, Altadena would look the same as it did before the fire,” one resident, who asked to remain anonymous, told the LA Times. “But it’s just not realistic.”

Many families are still tangled in insurance claims or simply lack the time and resources to start over. However, help may soon be on the way.

On June 12, the state will launch the CalAssist Mortgage Fund, which will provide up to $20,000 in grants to homeowners whose homes were destroyed or left uninhabitable by recent disasters, including the wildfires, California Gov. Gavin Newsom announced on Thursday.

“We know that recovery takes time, and the state is here to support,” Newsom said. “California is extending this ongoing support to disaster victims in Los Angeles and beyond, by assisting with mortgage payments to relieve financial pressure and stress as families rebuild and recover.”

Some displaced residents aren’t waiting. According to real estate agent Chelby Crawford, 10 percent of buyers at her open houses are Eaton fire victims looking to relocate.

“Pasadena and La Cañada Flintridge are benefiting the most,” she said. “Fire victims are just excited to find their next home. It’s selling season.”

Still, some are fearful of the rapid pace of redevelopment. Altadena is known for its century-old Craftsmans, Colonial Revivals and English Tudors. Residents fear new builds and gentrification will erase the town’s charm.

Others argue that development may be the only way forward. Brock Harris, a real estate agent who sold several burned lots, said it’s mostly small developers scooping up properties. These developers typically handle five to 10 builds a year.

“If Altadena is going to come back, we need way more developers coming in to help out,” Harris told the LA Times. “Otherwise, a decade from now, it’ll look desolate and unwelcoming with one house for every five lots.”

Email Richelle Hammiel

by Richelle Hammiel | Jun 6, 2025 | Industry, News Feed

In May, Elliman requested to move the dispute into an arbitration and provided all relevant agreements to Holly Parker’s claims, according to TRD. Parker withdrew the lawsuit without prejudice, meaning she can refile later.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Top-producing agent and longtime Douglas Elliman veteran Holly Parker has withdrawn her lawsuit against the brokerage, according to the New York County Clerk court filing.

Parker filed the suit back in April after Elliman demanded $1.5 million in clawbacks, including bonuses, assistant pay, advertising costs and StreetEasy fees. In return, Parker sought to void the clawback demand and recoup roughly $385,000 in damages and legal costs.

In May, Elliman requested to move the dispute into an arbitration, and in June, provided all agreements that govern the parties’ dispute. Parker withdrew the lawsuit, or discontinued it, without prejudice.

The legal dispute erupted following Parker’s February move to Compass after more than two decades with Elliman. At the time, Parker reportedly had 16 pending deals on the table. Under her 2020 independent contractor agreement (ICA), Parker was entitled to a 40 percent commission split on those deals, payable within 30 days of closing, the lawsuit states. That deadline came and went, and Parker claimed the firm still owed her nearly $193,000 after 10 of those deals closed.

Parker argued that side agreements she signed at Elliman should override her original contract. According to Parker, these agreements increased her commission split to 70 percent and included up to $205,000 in reimbursements and a performance bonus.

The lawsuit also stated, “As a matter of professional courtesy, Parker discussed her intentions to leave Elliman long before she effectuated the termination. Elliman never cited to Parker any clawback rights it believed it maintained and instead indicated to Parker that she would be paid for all pending transactions that closed within 90 days following her departure.”

Both Parker’s legal team and Douglas Elliman representatives declined to comment on the matter.

The dropped lawsuit follows a major leadership shakeup for Elliman, where Michael S. Liebowitz, the firm’s board director, took the reins as president and CEO after Howard Lorber announced his retirement.

A number of high-profile agents have also stepped away in recent months, including: Former head of Douglas Elliman’s Western Region operations Stephen Kotler and his son, Max Kotler who joined the Corcoran Group; Tinka Ellington and her team who left for Compass; and a group of six Aspen, Colorado-based Elliman agents who also signed on with Compass.

Email Richelle Hammiel

by Richelle Hammiel | Jun 3, 2025 | Industry, News Feed

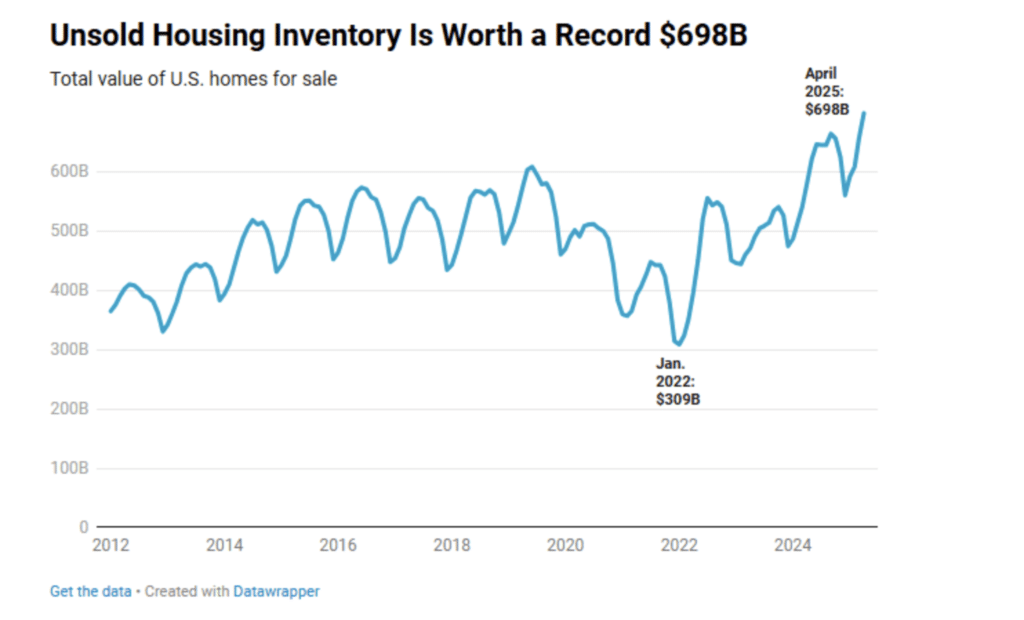

U.S. home inventory hit a record $698 billion in April, a 20.3 percent increase from the previous year. However, sales aren’t keeping pace, a new analysis from Redfin shows. While listings are rising, buyer activity remains muted, leaving many homes sitting unsold far longer than usual.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

U.S. home inventory hit a record $698 billion in April — a 20.3 percent increase from the previous year — but sales aren’t keeping pace, a new analysis from Redfin shows.

While listings are rising, buyer activity remains muted, leaving many homes sitting unsold far longer than usual.

Redfin | Unsold Housing Inventory

In April alone, total listings jumped 16.7 percent year over year, the highest level in five years, while new listings rose 8.6 percent, hitting a three-year high, yet buyers haven’t followed. Redfin reports there are now nearly 500,000 more sellers than buyers nationwide.

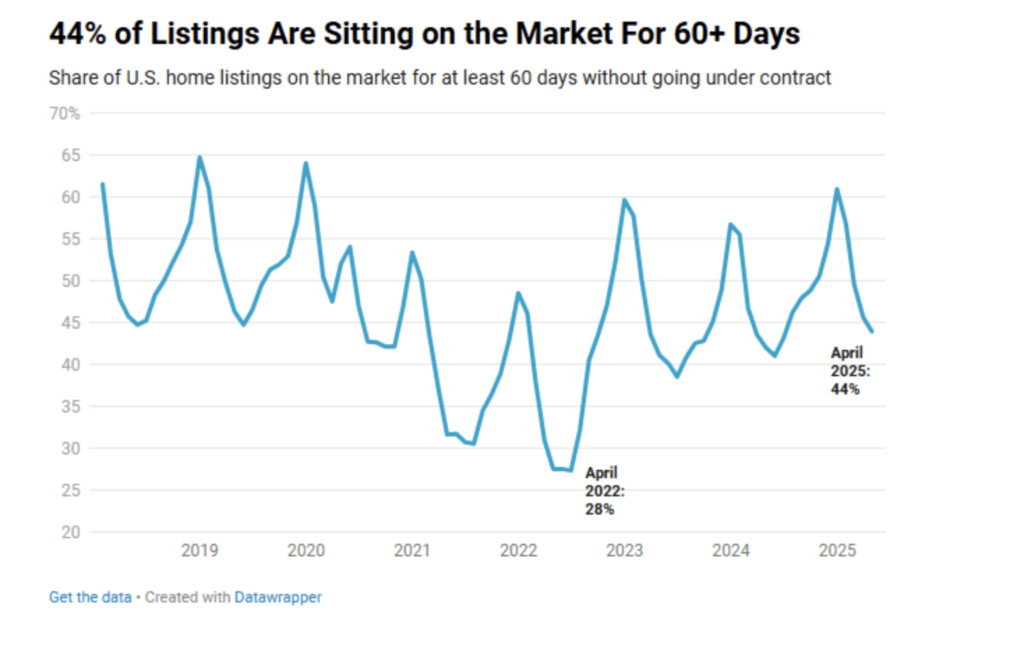

Homes are lingering on the market and getting stale. The typical home took 40 days to go under contract in April — five days longer than last year. More than 44 percent of listings were on the market for 60 days or more. That stale inventory alone accounts for $331 billion, nearly half the total market value.

Redfin

Chen Zhao | Redfin’s Head of Economics Research

“The record-high dollar value of all homes listed for sale is one way to quantify this buyer’s market,” Chen Zhao, Redfin’s head of economics research, said in Redfin’s analysis. “Not only are there more homes for sale than there have been in five years, but the value of those homes is higher than it has ever been.”

Contributing to this slowdown are record-high monthly housing costs, economic uncertainty and rising home-sale prices. The median U.S. home-sale price in April was up 1.4 percent from the previous year, but many sellers are now willing to negotiate.

“A huge pop of listings hit the market at the start of spring, and there weren’t enough buyers to go around,” Matt Purdy, a Redfin Premier agent in Denver, said. “House hunters are only buying if they absolutely have to, and even serious buyers are backing out of contracts more than they used to. Buyers have a window to get a deal; there’s still a surplus of inventory on the market, with sellers facing reality and willing to negotiate prices down.”

Matt Purdy | Redfin Premier Agent

In stark contrast to today’s slower market, inventory in early 2022 bottomed out at $309 billion. Mortgage rates hovered around 3 percent, and homes sold in a median of just 24 days. Now, with rates near 7 percent and affordability stretched thin, the stockpile of unsold homes keeps growing.

Zhao says there may be a silver lining for buyers as incomes continue to increase.

“We expect rising inventory, weakened demand, and the prevalence of stale supply to push home prices down 1 percent by the end of this year, which should improve affordability for buyers because incomes are still going up,” she said.

Email Richelle Hammiel