by Andrea V. Brambila | May 23, 2025 | Industry, News Feed

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Howard Hanna Real Estate Services CEO Howard “Hoby” Hanna told Inman his decision on Wednesday to send a missive to the National Association of Realtors and more than 70 MLSs informing them that his brokerage no longer considers NAR’s Clear Cooperation Policy binding was all about choice and innovation.

Inman immediately reached out for a phone interview to find out more and the conversation touched on nationwide and local MLS policies, antitrust risk, Zillow’s new private listing rule, possible fines for Howard Hanna brokers, the catalysts behind the CCP, fair housing, and how Howard Hanna’s parent company, Hanna Holdings, will handle CCP compliance by market.

TAKE THE INMAN INTEL INDEX SURVEY FOR MAY

“This is not about private or exclusive listing but more about trade associations mandating policies upon the industry that eliminate innovation creativity and unique marketing strategies that provide consumer choice regarding how their home is marketed,” Hanna told Inman in an email.

This interview has been edited for length and clarity.

Inman: Will you be having a dialogue with the MLSs that ask for it?

Hoby Hanna: Yeah. What I really think is MLSs should make their own rules in regards to participation that affect their members and have a voice, and not just take a policy that was written up top across the whole country and say, “This is how you have to do business,” and then makes all of us complicit in that form of business if we belong to the MLS.

To me that looks like antitrust, and that looks like we’re all having to do something if we want to participate. I think there should be individual participation rules.

Even in regards to this Zillow policy, Zillow is a broker in almost every MLS. They’re a participant like everybody else. One thing was when they said, “Well, you couldn’t display it on your website without [it] being on Zillow.” Well, that’s a far reach. Then you come back and say, “You can’t market it [on] anything, even if a seller requires it or that listing is banned for life.” It seems like that, in itself, is a pretty far reach and taking away consumer choice.

I’ve even said to some MLS executives, some of them should turn around and say to Zillow, “You can’t be a participant here and have our feed if you’re putting these stipulations on our members’ ability for seller choice.” If Zillow wants to say you can’t be on Zillow, but then they shouldn’t get the IDX feeds that they get everywhere.

The MLSs that said, “We have to follow NAR’s policy,” did they say, “We have to follow the policy, so we will levy fines or suspend members”?

They have not said that. I’m not even sure how they would collect the fines. But their answers were pretty straightforward: “We have our policies. They’re in conjunction with NAR and we expect that if you’re going to be a member here, that you participate to those policies and procedures.”

So what will Hanna Holdings do if its brokers are suspended because they don’t follow the policy, or if they levy fines? Are you going to pay the fines?

We won’t pay the fines. We don’t think our agents should pay the fines if the seller has choice. I’m saying that each MLS should have its own individual policies, and then we, as a broker and our separate franchises and in separate markets, will decide in those markets if we agree with those policies and how we’ll participate.

But if it’s just an adoption of Clear Cooperation, and they want to then turn around and fine on those policies and we have contracts that sellers don’t want to be privy to those policies, and they still want to fine us, we won’t pay the fines. For them, what does that lead to, if we don’t pay the fines? Then, okay, they’re going to say we can’t participate in the MLS? Well, is that really what they want to do? They want to have less inventory in the MLS? Do they want to destroy the MLS?

We could still put everything on our website and say to cooperative brokers, “You guys can come in, look at the homes here, and we’ll still cooperate with you,” because the MLS doesn’t offer cooperation anymore. There’s no offer of compensation; that’s been taken away. Cooperation is no longer offered as per the rulings and NAR settlement, we can’t offer cooperation. You have to find it. You can’t put it in the MLS to find out what it is.

It’s going to be your brokers, your franchisees, they’re going to get a notice saying, “You’re gonna have to pay this fine because you violated this policy,” so are you going to-

They’re going to have to decide individually what their reaction is at a franchise level. At a corporate level, we will decide when we talk to those different MLS executives and they say, “We’ve created our own participation policy, and this is what it is.”

We’ll decide, “Okay, that seems fair to us. That seems logical. You’ve given solutions that aren’t just to the 24-hour rule of Clear Cooperation. You’ve addressed seller choice.” So then we’ll decide individually, “Yes, that seems good to us, so we’ll be a member in good standing and abide by that,” and if there are fines in that case, we’ll pay the fines.

But just somebody blindly adopting NAR’s policy and saying we all have to abide by it, that we just can’t continue to do. That’s what got the industry in its last antitrust case.

It all stems back to MLSs specifically following rules that were mandated by NAR and then no brokers ever took a stance like this, saying, “We disagree with that. We’re separating ourselves from this. We’re giving our sellers and ourselves choice.”

We want to separate ourselves from the edicts of organized real estate.

So if your brokers decide to pay the fines, then that’s fine with you? If they make their agents pay, that’s fine with you?

Yes, they’ll make their overall decision. But as a holding company, we’re making it clear that we do not believe that Clear Cooperation as it exists is in the best interest of the industry or in the best interest of Howard Hanna being an innovative, technology-based leading broker.

We don’t think it captures seller choice if seller choice is disclosed. We do a pretty good job of making sure they understand their options. We think that just everybody blindly [following the policy] just puts too much exposure on future litigation.

You mentioned in the letter that CCP was adopted in response to fear that brokers were pursuing novel marketing strategies and taking advantage of new technologies. Why would NAR fear that?

Well, remember, it wasn’t just NAR. It was NAR’s MLS advisory board. A lot of the people that make up [that board], they’re not the leading brokerage firms in the country. There were people who were worried about Compass’s exclusive listing model. They were worried about programs like our Find It First, which allowed people to come search [listings before they were posted in the MLS]. They were worried about new entrants that said, “I don’t need an MLS.”

It’s just there was so much technology happening and plenty of people got scared of the status quo being disrupted.

So you’re saying it’s not NAR that’s fearing these new strategies, it’s the people on the MLS advisory board and committee?

Which, therefore, NAR sanctioned it, supported it, and said, “We are pushing this down to that three-legged stool,” saying you have to operate with this new rule.

And why would NAR do that?

I don’t know. In 2020, I never understood why they passed Clear Cooperation.

Well, I was there in the meetings at the time, and the big thing seemed to be fair housing.

I heard that too, and I looked at people and said, for example, if Howard Hanna left the MLS and our seller said to us, “We don’t need MLS. We think you guys do a great job, and you’ve got a website, and you’ve agreed to put our listing on HowardHanna.com” and let’s say we agreed to put it on Zillow and Realtor.com. Let’s just say that was our business model. Would that be a violation of fair housing?

And if there’s logic in that, if a seller wants to sell their own home, why don’t they have to put their house on Zillow, or put their house in a multi-list? These multi-lists and Zillow aren’t public utilities. Why does a builder not have to put the house in the multi-list? Are they violating fair housing? I just think that’s like one of those scare tactics.

If you could prove to me that HowardHanna.com doesn’t allow people of color or minorities or those affected by fair housing to look at our website — that doesn’t make sense to me. Maybe I’m wrong. Does that make sense to you that you have to be in the MLS to offer fair housing?

I think the idea at the time was, if you put it in the MLS, it goes out to not just HowardHanna.com but it goes out to all these other brokerage websites. It goes out to all the brokers and agents in the market. And so the maximum number of people will be able to see the listing, and not just the people that know to go to HowardHanna.com or the people that know a Howard Hanna broker or agent.

Ok, but under that same logic, if you’re a homebuilder, they don’t have to be in the MLS, and they don’t share their listings together. They choose if they’re going to put their listings online or partner with Zillow or give a feed.

My argument isn’t about holding all your listings off. It’s not about a three-phase marketing plan. It’s about if a seller wants to have choice, or you can create innovation or somebody in the industry could come up with a better way to display, share, promulgate their business, or somebody doesn’t want to have their house on the market in 24 hours.

It’s these unintended consequences. It’s not about not sharing inventory. It’s just, don’t put such stipulations and rules on it. I don’t think it’s a violation of fair housing. If the government wants to, [it can] say, “We think there should be a public utility, and whether you’re an individual homeowner or builder, developer, Realtor, everybody has to put their listing for sale on the public utility for everybody to see.”

We’re taking this position to distance ourselves a little bit from this organized real estate mandating what everybody else does. We actually think other people should take a hard look.

Do you know if any other brokerages have sent similar letters to NAR or MLSs?

I do not, and I didn’t talk to any brokers prior to doing this. This was our choice and our decision. We haven’t consulted, asked, gone into a coalition. We just said this is where we, as an independent business, feel we need to be.

At the end of the letter, it says Hanna Holdings and its affiliates and franchisees will determine, on a market to market by market basis, whether to require the listing brokers to submit listings on an MLS within one business day of marketing. How will Hanna Holdings determine whether to require that?

We will leave it up independently to our local markets and our franchisees, after discussion with MLSs, and let them make [the decision] but we’re not mandating that they have to operate in that sense. Sort of like we don’t mandate that you have to be a member of the National Association of Realtors to work at Hanna Holdings or any of its subsidiaries.

Email Andrea V. Brambila.

Like me on Facebook | Follow me on Twitter

This post was originally published on this site

by Andrea V. Brambila | May 23, 2025 | Industry, News Feed

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

This story will be followed later today with an interview with Howard Hanna Real Estate Services CEO Howard “Hoby” Hanna IV. Check back in a little bit.

Howard Hanna Real Estate Services is drawing a line in the sand.

On Wednesday evening, company CEO Howard “Hoby” Hanna IV sent a letter to the National Association of Realtors and more than 70 multiple listing services the brokerage belongs to, informing them it will no longer consider itself bound by the organization’s Clear Cooperation Policy, Inman has learned exclusively.

TAKE THE INMAN INTEL SURVEY FOR MAY

The policy requires brokers to submit listings to the Realtor-affiliated MLSs they belong to within one business day of marketing to the public. After months of consideration and vigorous debate across the industry, NAR chose in March to keep the policy as-is while adding a new delayed marketing option for sellers.

But it wasn’t enough. In the letter, Hanna describes Clear Cooperation as “bad policy” that Hanna Holdings — Howard Hanna’s parent company — never agreed to and voted against when it was adopted in 2020. “It deters innovation in the industry by restricting how Realtors market homes,” he wrote in the letter.

“Indeed, it was adopted in response to a fear that brokers were pursuing novel marketing strategies and taking advantage of new technologies. Stamping down on that innovation harms brokerages and it harms their customers.”

NAR, the letter continues, should not dictate how brokerages conduct business.

“Hanna Holdings does not consider the Clear Cooperation Policy binding and, accordingly, no Hanna Holdings affiliate or franchisee will adhere to the policy as a matter of course,” Hanna wrote.

“Instead, Hanna Holdings and its affiliates and franchisees will determine on a market-by-market basis whether to require their listing brokers to submit listings on a multiple listing service within one business day of marketing the property to the public.

“It will make these decisions based on its own business interests and independent of NAR and of any other brokerage.”

In a statement, a NAR spokesperson told Inman, “Clear Cooperation remains a mandatory policy, and MLSs are responsible for enforcing MLS policies. By joining a Realtor association-owned MLS, participants and subscribers agree to comply with the MLS rules and regulations.”

NAR did not respond to questions asking whether there will be any consequences for the company or its brokers if they don’t follow the policy, whether NAR will be taking any action as a result of the letter, whether any other brokerages have informed NAR they won’t follow the mandate, whether NAR had responded to Hanna’s letter and when NAR planned to respond.

Hanna told Inman in a phone interview that he called NAR CEO Nykia Wright before sending her and NAR’s chief legal counsel the letter and said it was “a very cordial call.”

“I said, ‘I just felt that [it was] probably better to make you aware of the situation, rather than just getting a blind letter,’ and she appreciated the call ahead of time, but we haven’t heard anything back,” Hanna said.

He said some MLS executives, such as those at West Penn MLS in Pennsylvania, Bright MLS in the Mid-Atlantic region and MLS Now in Ohio, had responded that they “want to have some dialogue,” while others, such as the Charlottesville Area Association of Realtors MLS in Virginia and a small MLS in North Carolina, had said “that they have to do whatever NAR tells them.”

Hanna told Inman that that doesn’t make sense to him.

“We have to make independent decisions, not just follow suit,” he said. “That’s what gets industries in trouble.”

Looming large in Hanna’s mind is that Howard Hanna was one of more than 90 large brokerages that were not covered under NAR’s $418 million settlement of multiple commission-related antitrust lawsuits nationwide last year, which meant that the company had to fight, and then settle, litigation it otherwise would not have.

Hanna believes MLSs should make their own participation rules rather than adopting a nationwide policy from NAR that mandates a particular way of doing business.

“[That] makes all of us complicit in that form of business if we belong to MLS,” he said. “To me, that looks like antitrust, and that looks like we’re all having to do something if we want to participate. I think there should be individual participation rules.”

None of the MLSs who said they had to follow NAR’s rules had thus far threatened fines, according to Hanna. But MLSs across the country have instituted hefty fines, some in the thousands of dollars, for violations of the CCP.

“We won’t pay the fines,” Hanna said. “We don’t think our agents should pay the fines if a seller has choice.

“What does that lead to, if we don’t pay the fines, then, okay, they’re going to say we can’t participate in the MLS? Well, is that really what they want to do? They want to have less inventory in the MLS? Do they want to destroy the MLS?”

Hanna has previously said his company was considering leaving the MLS due to NAR’s mandatory MLS policies.

“We could still put everything on our website and say to cooperative brokers, you guys can come in, look at the homes here, and we’ll still cooperate with you,” Hanna said.

The company would leave it up to its brokers whether to follow the CCP and whether to pay the fines or require their agents to pay the fines if they choose not to, according to Hanna.

“They make their overall decision,” Hanna said.

“But as a holding company, we’re making it clear that we do not believe that Clear Cooperation as it exists is in the best interest of the industry or in the best interest of Howard Hanna being an innovative, technology-based leading broker.

“We don’t think it captures seller choice if seller choice is disclosed. We do a pretty good job of making sure they understand their options. And we think that just everybody blindly [following the policy] just puts too much exposure on future litigation.”

Read the letter (re-load page if document is not visible):

Email Andrea V. Brambila.

Like me on Facebook | Follow me on Twitter

This post was originally published on this site

by Andrea V. Brambila | May 22, 2025 | Industry, News Feed

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

The buyer of a Los Angeles home that formerly belonged to a serial killer known as “The Grim Sleeper” has put the home on the market and simultaneously sued the home’s sellers and every agent and real estate company involved with the purchase for allegedly not disclosing the home’s previous notorious occupant.

The murderer, Lonnie David Franklin Jr., was convicted in 2016 of killing nine women and a teenage girl between 1985 and 2007 in Los Angeles and was suspected of killing many others over his lifetime. He was sentenced to California’s death row, but died in prison at age 67 in March 2020.

TAKE THE INMAN INTEL SURVEY FOR MAY

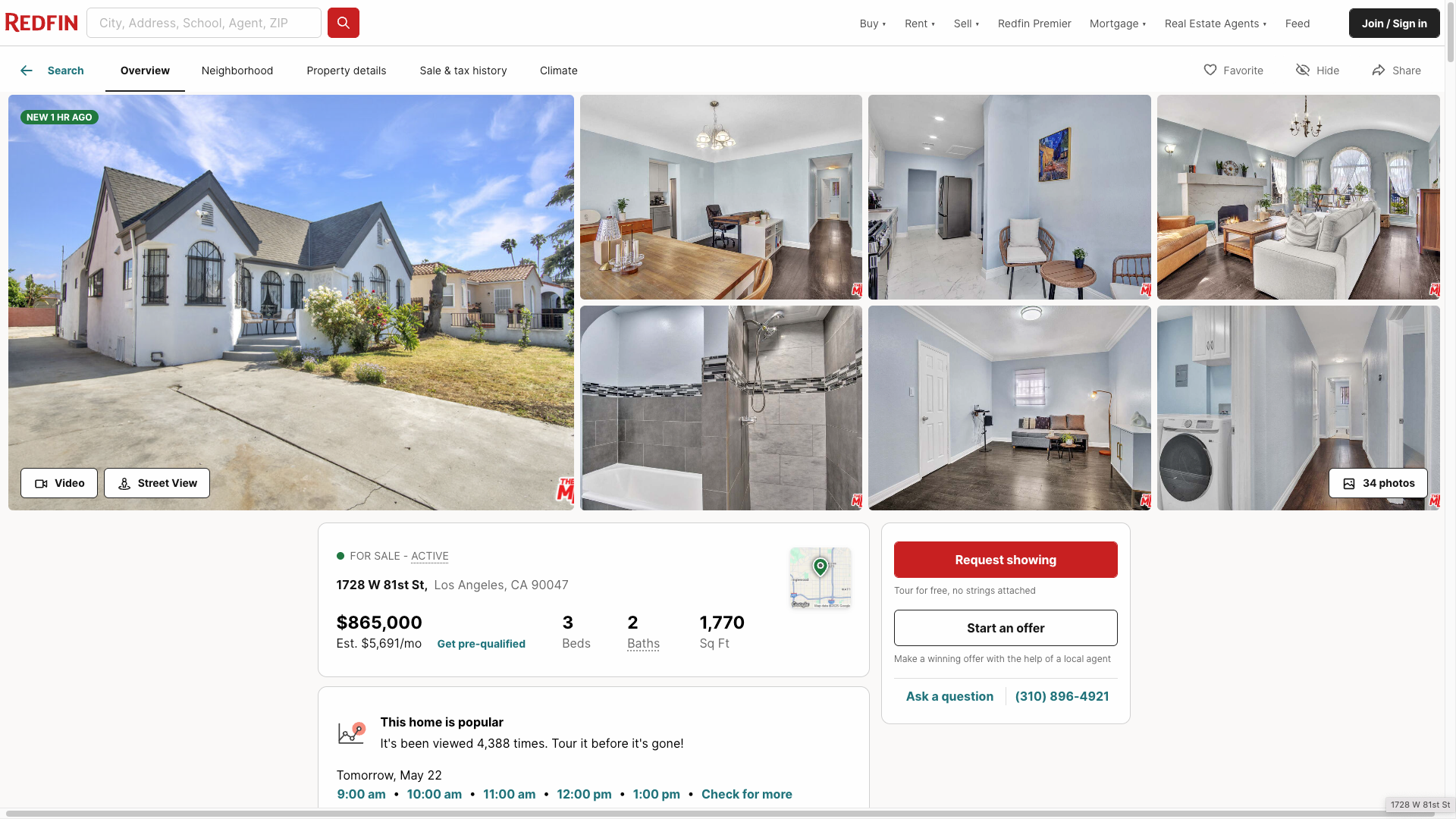

Franklin’s former home, located at 1728 West 81st Street in Los Angeles, was put up for sale on Wed. May 21, according to Redfin’s website. The three-bedroom, two-bathroom 1,770-square-foot house was listed for $865,000.

“The spacious dining and living areas boast a cozy fireplace, while abundant storage cabinets and pantries add to the home’s functionality,” the property’s listing description reads.

“Step outside to the covered patio, ideal for relaxing or hosting guests.”

A Redfin listing for the property at 1728 W. 81st St. once owned by “The Grim Sleeper,” Lonnie David Franklin Jr. The listing was uploaded to Redfin on May 21, 2025.

The listing description makes no mention of the home’s previous occupants or the legal imbroglio surrounding the home. Inman has reached out to the listing agent, Joseph M. Rasson of Rasson Realty & Financial Corp., for comment and will update this story if and when a response is received.

On Mon., May 19, the most recent buyer of the home, Suyeon Park, filed a lawsuit against sellers Surendra Pandey and Madav Budhathoki; Khemlal Adhikari, the listing agent; Keller Williams Coastal Properties, the listing brokerage; Jason Anderson, the buyer’s agent; eXp Realty of California, the buyer’s brokerage; Pacific Coastline Escrow, the escrow company for the transaction; and Chicago Title Company, the title company for the transaction.

Park bought the home in February 2025 for about $755,000.

The suit, filed in the state’s Los Angeles Superior Court, accuses the defendants of “sheer laziness in order to make a quick profit” and maintains they knew the house was once owned and lived in by The Grim Sleeper.

“The Grim Sleeper resided at the House during the entire murder spree,” the complaint says.

“Defendants knew that Plaintiff was not aware of this. But either negligently, purposely, knowingly and/or intentionally failed to disclose this information in order for the Transaction to go through and have them get paid.”

“Defendants knew that the House was nowhere near the value of which it was sold to Plaintiff given that a serial killer lived there,” the complaint adds, noting that the defendants assured Park before the deal closed “that there was nothing that Plaintiff needed to be concerned with relating to the House.”

The complaint alleges that when Park moved in, she made improvements to the house costing about $50,000.

A neighbor informed Park that the house was once owned by The Grim Sleeper and when Park asked the neighbor whether the sellers knew, the neighbor said the sellers knew, according to the complaint.

The neighbor also allegedly told Park that the house had once been listed, then taken off the market and re-listed again “after some time” at a “significantly lower price.” The same neighbor also mentioned an incident during an open house when a car drove by and yelled to Adhikari, the listing agent, that the house was where The Grim Sleeper had lived.

The complaint also describes an incident toward the end of February 2025 after Park moved in when a technician came to the property to install internet.

“Unknown to Plaintiff, another passerby drove and parked his vehicle and then approached the technician if he could take a tour of the House given that a serial murderer had lived there,” the complaint says.

“As a result, Plaintiff has lived with constant fear and stress for her safety and well being.”

The complaint makes 10 claims against the defendants: breach of implied covenant of good faith and fair dealings; intentional misrepresentation; concealment; negligent misrepresentation; fraud; conspiracy to defraud; breach of fiduciary duty; constructive fraud; intentional infliction of emotional distress; and negligence.

The filing charges that “there existed an implied promise that Defendants make full disclosures as to issues relating to trespassers and deranged fans of the serial killer that used to live there” and that “in order to reap all the benefits of the Transaction, Defendants purposely did not disclose that a serial murder lived there and that Plaintiff may be bombarded with unwelcome guests.”

The complaint stresses that Park would not have bought the home “[h]ad Defendants disclosed this omitted information.”

The complaint asks for compensatory damages, exemplary and punitive damages, and for attorney’s fees.

Inman has reached out to the defendant agents and companies for comment and will update this story if and when responses are received.

Read the complaint (re-load the page if document is not visible):

Email Andrea V. Brambila.

Like me on Facebook | Follow me on Twitter

This post was originally published on this site

by Andrea V. Brambila | May 16, 2025 | Industry, News Feed

The Federal Reserve analysis found that rising home prices are likely why commission rates fell in the past two decades, but found no impact on rates after buyer contracts were required in 15 states.

Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

One of the primary changes instituted by the National Association of Realtors’ nationwide antitrust settlement may end up having no effect on commission rates, according to an analysis by the Federal Reserve released this week.

The analysis, “Commissions and Omissions: Trends in Real Estate Broker Compensation,” examined commission rates advertised to buyers’ agents in a dataset of real estate listings from CoreLogic covering about half of properties listed nationwide from 1995 to 2023.

The researchers also used the CoreLogic House Price Index and average resale prices from CoreLogic Market Trends to look at the relationship between commissions and home prices and gathered data on buyer representation agreements and rebate bans from state legislative archives.

Buyer representation agreements lay out buyer and agent responsibilities, agency representation and agent compensation details. They are required by 15 states, before and independent of the NAR settlement, which requires buyer agents to sign agreements with buyers they are working with before showing them a home.

The study’s authors, Rupkatha Banerjee and Andrew Paciorek, found that commission rates have come down a bit nationally over the past two decades, from an average of about 3 percent in the late 1990s to about 2.7 percent in 2023. There also appears to be slightly more variation: In 2002, commissions largely clustered at 3 percent, while 20 years later, there was more of a spread, with more 2.5 percent and 2 percent rates.

“The highest bar is still at 3, suggesting that the industry norm of the 6 percent total commission paid to buyer and seller agents persists to some extent, at least under the usual assumption that the buyer and seller agents split commissions equally,” the researchers wrote.

“This persistence may be explained by steering and how poorly low-commission properties fare. Low commission listings stay on the market for longer and are less likely to sell,” they said, citing a 2019 study.

“Brokerage firms that offer low commissions are less likely to obtain cooperation from agents from larger firms, who make up the majority of the real estate market,” they added, citing a 2017 study.

“Thus, they are unable to compete with full-commission brokerage agencies.”

The researchers found that median home prices have nearly doubled since 1995 and that, when taking into account home prices, the downward trend in commission rates goes away.

“The variation in rates across metropolitan areas is negatively correlated with house prices, and we find that controlling for house prices in a panel regression eliminates the downward time trend,” the researchers wrote.

“Moreover, the magnitude of the correlation between house prices and commission rates implies that rising house prices could explain more than half of the aggregate trend.”

They theorized that the increase in home prices insulated agents from the effects of lower rates.

“When house prices are higher relative to consumer prices or prevailing incomes, real estate agents may be more willing to work for lower commission rates, since the higher selling price offsets the lower rate,” the researchers wrote.

The researchers also looked at commission rates in the years before and after buyer representation agreements and rebate bans were put in place in different state. They controlled for home prices to isolate the effects of the policies.

“Interestingly, we find no material or statistically significant effects of buyer representation agreement requirements or buyer rebate bans on advertised commission rates, suggesting that changes in these policies might not have a material effect,” the researchers wrote.

The researchers acknowledge that the NAR settlement includes a new provision not present in the states analyzed: The prohibition on advertising commission rates to buyers’ agents through the multiple listing service. This, they said, “could mitigate the issues of steering and collusion” and “lead to more substantial changes to business models and agent commissions going forward.”

Still, they noted that listing agents had found workarounds around the settlement’s prohibition and that NAR had added an option to delay marketing listings on top of its Clear Cooperation Policy (CCP), which requires listing brokers to submit a listing to the MLS within one business day of publicly marketing it.

“[P]ress reports suggest that sellers’ agents have found ways of sharing information on commission rate offers outside of the MLS,” they wrote.

“In addition, the NAR has relaxed its Clear Cooperation Policy, leaving more freedom for listing agents to forego or delay listing a property on the MLS in the first place. These sorts of adaptations make it difficult to predict the long-run effects of the settlement.”

Email Andrea V. Brambila.

Like me on Facebook | Follow me on Twitter

This post was originally published on this site

by Andrea V. Brambila | May 5, 2025 | Industry, News Feed

This is the first in a two-part interview with Howard Hanna Real Estate Services CEO Howard “Hoby” Hanna IV. The interview was conducted in the weeks leading up to the independent brokerage’s settlement on May 2 in the Gibson antitrust commission lawsuit. Read the first part HERE.

In choosing to keep its pocket listing rule and add a new delayed marketing option, the National Association of Realtors has been accused of trying to mollify its biggest broker members.

Did it work? Not according to Howard W. “Hoby” Hanna IV, the CEO of Howard Hanna Real Estate Services.

Inman reached out to Hanna last month to ask how NAR’s new Delayed Marketing Exempt Listings category might impact Howard Hanna’s listing displays. The 1.5-million-member trade group added the category after choosing to keep the Clear Cooperation Policy, a controversial rule that requires listing brokers to submit listings to Realtor-affiliated multiple listing services within one business day of publicly marketing them.

NAR’s new listing category allows brokers to keep listings off of MLS subscribers’ Internet Data Exchange (IDX) listing websites, but not Virtual Office Websites (VOWs), which require registration in order to see certain information.

Hanna told Inman that as a result of the change, Howard Hanna is “seriously considering moving to registration in all markets” and is looking at options to re-launch its Find It First program for listings that had not yet been entered into the MLS as well as for sellers choosing to keep their listings off of the MLS altogether.

According to Hanna, Howard Hanna first tested a VOW in the summer of 2023 in the Cleveland area in Northeast Ohio, where the company has a big market share, and the move resulted in increased traffic and better lead generation with more qualified leads.

“We have not moved completely to all markets but are now looking with pure intent to maximize our customer experience and create the best consumer experience for buyers and sellers,” Hanna told Inman in a statement.

“We also think our Buy & Borrow Bundle with Find it First will tie into creating a great experience for the clients that choose Howard Hanna.”

The company’s Buy & Borrow Bundle offers a closing cost credit of 0.5 percent of a buyer’s loan amount — up to $10,000 — for qualified buyers who choose to buy their home with Howard Hanna and also get a mortgage with Howard Hanna Mortgage Services.

But Hanna also offered his thoughts on long-term changes he’s contemplating for the company, including the potentially industry-changing step of leaving NAR and its affiliated MLSs.

This interview has been edited for length and clarity.

Inman: Some say that VOWs present a registration hurdle that people might not want to bother with when they’re searching websites for listings; they may see the registration requirement and leave. Is that not something you’re concerned about? You also mentioned the customer experience — how is that a better experience?

Hoby Hanna: How many retail, consumer-based websites are you personally registered on so that you get a deeper level of retail experience? You can get Nordstrom’s customers to sign up, and they have your information, and you’ll get information about bonus days, new items, new luxury goods and other things because you’re a customer before the general public does.

If [a customer] can know about the market earlier, faster, quicker and know about special items before everybody else, that doesn’t hurt the market. It just makes those of us who may offer that experience pick up more clients and have the ability to cross-market different products and other things. So I’m not as concerned.

You mentioned before how having these Find It First listings helps with stickiness — people go to your website to see the latest listings. The new policy around Delayed Marketing Exempt Listings allows you to have those listings in your VOW, right? So if other brokers, which at this point also include Redfin and Zillow, have VOW sites, it means they can display these delayed marketing listings as well. How do you feel about that?

That’s part of the competition, and they can do that. I actually think that’s another proverbial shoe that’s gonna drop. Whether you want to do it as a VOW feed and have those there, or whether you don’t and go away from a VOW and make it more just that you’re gonna get our Find It First or [office] exclusives, all you have to do is register.

We’re having conversations with people both at Zillow and Redfin because if we go to everything Find It First and exclusives and not feed from VOW or IDX at all with those listings, they’re not gonna have them. They want to make sure they can still showcase our listings for their business model that they may have to change, and maybe they have to pay for those listings in some capacity, as opposed to just receiving them through an MLS feed.

I’d be willing to send them that if they’re willing to accept it and maybe work a deal out where they’re giving us our leads back on those and not monetizing them to other partners if they want that ability for a period of time.

What is it that you can do that would prevent Zillow and Redfin from getting your listings? What is it that they’re bargaining with you for?

I won’t put them in a VOW. I won’t have a VOW. I don’t need a VOW. I don’t need IDX. I might not be in MLS anymore. The world’s changed. I don’t need to listen to NAR. There might not be MLS five years from now, if people are going to dictate where I have to send things.

Quite honestly, this rule that they changed, the thing’s called Clear Cooperation. We don’t need to cooperate with each other anymore. That was taken away by the lawyers.

We love to cooperate with other brokers. We love to share our data and our listings, those that the seller says, “Fine, put it into the open market and share.” But if we want to [we can] put everything on our website and say to the consumer, “We don’t put it in an MLS anymore. We do direct feeds to Zillow. We do direct feeds to Realtor.com. We have it on our website. We send a letter to every broker in the country and say you’re still welcome to show a house.”

We’re not going to follow rules based on NAR telling us how to operate our business. That’s not the role NAR should play.

Is that your plan?

I’m considering it.

Email Andrea V. Brambila.

Like me on Facebook | Follow me on Twitter

This post was originally published on this site